Aave is evolving from a lending protocol into a core Web3 financial infrastructure pillar. This article analyzes its growth drivers, revenue model, and the silent competition among lending platforms like Aave, Compound, and Morpho.

Aave: The Evolution of a Financial Structure

The lending market is one of the first and most core applications of DeFi, serving as a source of liquidity and leverage for the entire ecosystem. After the initial boom with protocols like Compound and MakerDAO, the DeFi lending sector entered a restructuring phase where capital efficiency, integration capabilities, and value distribution mechanisms became core competitive factors.

Among these, Aave is one of the rare lending protocols that has not only adapted to this transition but has also redefined the credit structure in DeFi by building a programmable and scalable infrastructure layer. As of mid-2025, Aave has recorded over $30 billion in Total Value Locked (TVL), accounting for nearly 50% of the DeFi lending market share, according to data from DefiLlama.

Aave began in 2017 as ETHLend, a P2P lending application on Ethereum that allowed users to match lending and borrowing orders directly via smart contracts. Despite its groundbreaking idea, ETHLend quickly ran into limitations regarding liquidity, matching efficiency, and user experience (UX), all of which reflected a reality: the global credit market cannot operate optimally based solely on two-way order matching. In 2020, the team completely restructured the product and launched Aave, shifting from the P2P model to pool-based lending. In this model, users deposit assets into liquidity pools and can borrow instantly against their collateral. This approach unlocked scalable liquidity, reduced latency, and paved the way for Aave to become a standard infrastructure for DeFi lending protocols.

Aave V1 & V2: The Flash Loans Architecture that Made Aave's Name

Flash loans are a borrowing mechanism that exists only within a smart contract environment, where users can temporarily borrow a large amount of an asset without collateral, on the condition that it is repaid within the same transaction. The transaction will automatically revert if the repayment conditions are not met. This feature emerged on Aave in its early stages (V1 and V2) as a natural consequence of the pool-based lending model: instead of matching each loan with a specific lender (P2P), assets are pooled together and can be temporarily used as long as it does not affect the system's immediate liquidity.

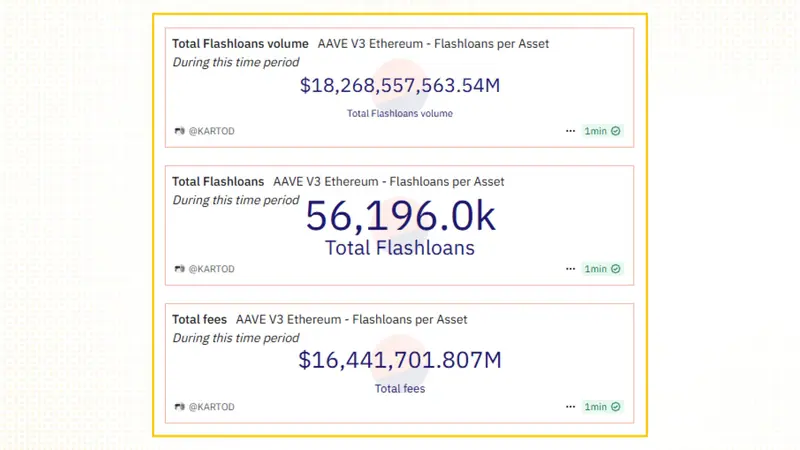

Flash loans are not aimed at the general public but primarily serve technical needs within DeFi: arbitrage, liquidation, restructuring debt portfolios between protocols, or moving borrowing positions. In an ecosystem where capital can be programmed, creating such temporary liquidity layers is a natural evolution. However, this mechanism was also exploited in several DeFi attacks from 2020-2021, which shows that flash loans should be viewed as an infrastructure tool, not a competitive advantage. Aave wasn't the only one to support flash loans, but it was the first protocol to deploy it at scale and has recorded consistent usage data over time. As of mid-2025, Aave has recorded over $18 billion in flash loan volume, generating over $16 million in revenue. While this figure is insignificant compared to its TVL, it reflects a specialized liquidity layer that can be leveraged in more complex DeFi products.

Aave V3: Upgrading the Structure for Risk Control and Profit Expansion

Following V1 and V2, the Aave V3 update launched in 2022 further restructured how capital is managed within the protocol, with the goals of: increasing capital efficiency, expanding listed assets without increasing systemic risk, and consolidating liquidity across multiple chains into a single layer through three approaches: eMode, Isolation Mode, and Cross-chain Portals.

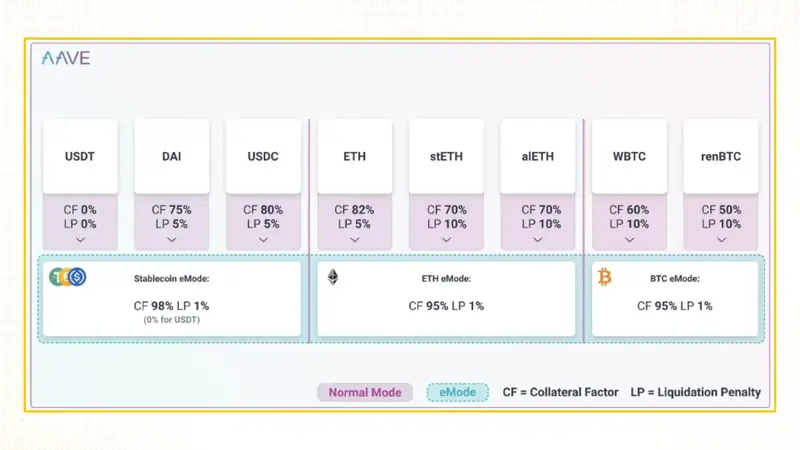

eMode: Optimizing LTV with High-Correlation Assets

eMode (High Efficiency Mode) allows users to borrow with a higher LTV (Loan-to-Value) ratio if their collateral and borrowed asset have a strong price correlation, which is typically applied to stablecoins. This is how Aave segments asset risk, instead of applying a conservative LTV threshold for the entire market. From a system perspective, eMode helps increase the total borrowed value, expanding interest-based revenue without significantly increasing the likelihood of liquidation. This is particularly suitable for institutions, stablecoin protocols, or DeFi applications that need leverage but require low borrowing costs and stable liquidity.

Isolation Mode: Enhancing Security for New Asset Listings

Isolation Mode allows the listing of high-risk tokens (e.g., newly launched, highly volatile tokens) without affecting the entire system. These assets can only be borrowed against a whitelisted stablecoin and have a low LTV limit. Instead of choosing between expansion and safety, Isolation Mode allows Aave to do both: it can attract TVL from new ecosystems (Layer 2s, appchains, RWAs...) while maintaining the system's protective layer. This is a critical difference from older-generation lending protocols.

Cross-chain Portal: Consolidating Liquidity Across Networks

Aave now operates on multiple blockchains (Ethereum, Polygon, Avalanche, Base...), but instead of fragmenting liquidity across each version, the Cross-chain Portal allows users to move assets and borrowing positions between chains. This approach helps maintain a single, aggregated liquidity layer, increasing capital efficiency and mitigating liquidity fragmentation—a common problem for current multi-chain protocols. Simultaneously, moving positions cross-chain reduces transaction costs, enhances user experience, and expands the overall profit margin.

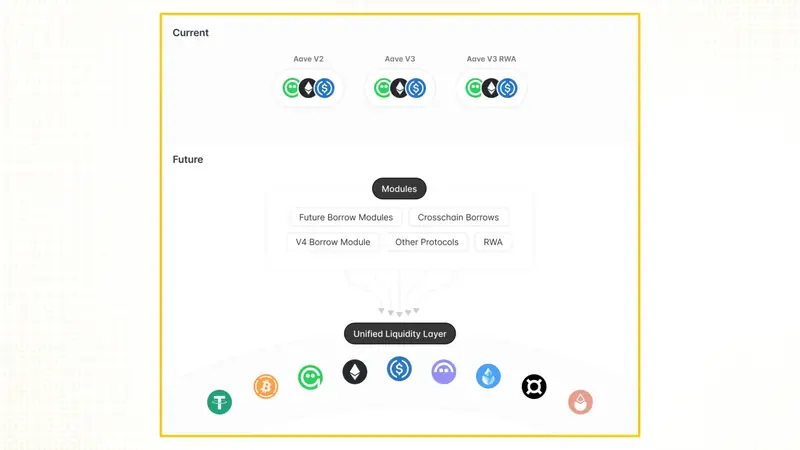

Aave V4: Redefining Architecture with a Hub-and-Spoke Model

If Aave V3 was an effort to optimize capital efficiency and security, Aave V4 (expected Q3/2025) is an architectural leap forward, moving towards a true modular finance model. The protocol will transition to a Hub-and-Spoke structure, where liquidity and risk data are consolidated into a central Hub, while credit products are deployed as specialized spokes optimized for specific use cases.

In the central layer, the Hub will be responsible for managing overall liquidity, systemic risk, and general parameters. From there, Aave can expand into Spokes such as:

- eMode Spoke: Optimized for stablecoins, pushing LTV to the maximum, suitable for institutional capital flows.

- Isolation Mode Spoke: Serving new or high-risk tokens, while keeping the system safe.

- RWA Spoke: A bridge to traditional assets like bonds, invoices, and tokenized real estate.

- Vault Spoke: Where DAOs or institutions can design customized lending strategies, expanding the on-chain structured credit market.

Each Spoke can operate as a verticalized revenue stream—a specialized profit stream that still uses the same liquidity layer, risk data, and security from the Hub. This allows Aave to expand both in depth (product customization) and breadth (user diversity) without sacrificing operational efficiency or risk control.

This layered architecture is accompanied by a Unified Liquidity Layer: a solution to the problem of fragmented capital across many chains and small pools. Instead of operating as separate entities, liquidity is now consolidated into the Hub and flexibly distributed among the Spokes. This not only helps improve capital efficiency per unit of TVL but also increases yield for LPs, reduces opportunity costs, and enhances cross-chain integration.

More importantly, Aave V4 opens up the possibility for third parties to build their own credit markets on top of Aave's architecture—like a kind of "Aave-as-a-Service." TradFi institutions, DeFi protocols, or DAO communities can deploy an independent Spoke, inheriting the security, liquidity, and risk governance from the Aave Hub. This creates a horizontal expansion model where Aave does not need to directly manage each market but still captures value through infrastructure fees, shared cash flows, or increased demand for the AAVE token and the GHO stablecoin.

Aave's Operational Model

Aave operates on a pool-based lending model: users deposit assets into pools to earn interest, and borrowers can collateralize assets to withdraw funds from those same pools. Everything is automated by smart contracts—from determining LTV, calculating interest rates, to handling liquidations—without any traditional credit assessment.

Aave's operational mechanism is based on two main components:

- aTokens: When users deposit an asset into a pool, they receive an aToken in return (e.g., aUSDC), which represents their deposit and automatically accumulates interest.

- Collateralized Borrowing: Users collateralize assets with an LTV of 50-85% and can borrow other tokens within the same system. Risk management (asset price, liquidation, interest rates) is entirely automated through pre-set parameters, with no manual review.

The decentralized nature is evident in how Aave has designed the entire process: from determining safe borrowing levels, handling liquidations, to distributing interest, everything is programmed on-chain and overseen by the DAO. There are no credit scores, no intermediaries. Risk is controlled by collateral and algorithms. A crucial component of the system is the Safety Module, where AAVE token holders can stake their tokens to contribute to a liquidity insurance fund. In the event of a system-wide insolvency, assets from this module can be used to cover a portion of the losses.

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Please do your own research before making investment decisions.