Global financial markets have entered an optimistic phase, with US stocks hitting new highs, Bitcoin surpassing $115,000, and capital continuing to flow strongly into ETFs. A stable CPI report, coupled with signs of a weakening labor market, solidifies expectations that the Fed will soon begin a cycle of interest rate cuts.

Market Overview

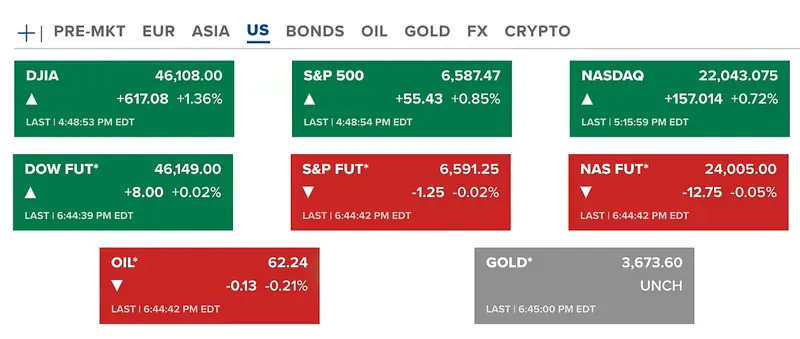

On Thursday (September 11th, US), US equities closed with gains across all three indices, with the Dow Jones rising the most at 1.36% and the S&P 500 setting a new all-time high. Stock futures were largely flat. Oil contracts saw a slight decrease to $62.2 per barrel. Gold remained high at $3673 per ounce.

Bitcoin's price briefly surged to $115,000. Most altcoins saw gains. The overall crypto market capitalization increased to $4.1 trillion.

US BTC spot ETFs continued to see positive inflows, with a total of $552.7 million on Thursday. ETH spot ETFs also had significant inflows of $113.1 million. This robust capital inflow into crypto ETFs indicates sustained institutional demand.

CPI Data Reinforces Rate Cut Expectations

The US CPI for this month saw a slight increase to 2.9% from 2.7% previously, which was in line with market forecasts. Meanwhile, Core CPI remained at 3.1%, matching expectations. The stability in Core CPI is a positive signal, as this is the index the Fed pays the most attention to.

Despite the slight increase in CPI, the market was not surprised and maintained a positive outlook. Tariffs were previously seen as the main risk that could cause inflation to rise again, but their impact has not been evident over the past four months. In the context of a weakening labor market, this data is considered the final piece of information before the Fed meeting on September 17th. There is an almost certain expectation that the Fed will hold interest rates steady.

Additionally, data from TrueFlation—a private company that is said to reflect official figures about 45 days in advance—suggests that inflation might see a slight increase, then decrease and stabilize around 2–3% in the coming months. This reinforces the view that inflation is currently on a stable trend, with no risk of a major resurgence. The financial market is becoming optimistic after the CPI report, as it strengthens the expectation that the Fed will begin its interest rate cutting cycle in September, with the possibility of four consecutive cuts until January 2025, totaling about 1%. The market is now almost certain the Fed will reduce rates by 0.25% at its next meeting, though there is still a small probability of a 0.5% cut. Furthermore, investors expect two more cuts in October and December, for a total of three rate reductions this year.

First-time US jobless claims rose to 263,000, higher than the 235,000 forecast and last week's 237,000, indicating a weakening labor market. This is a crucial factor the Fed will have to consider, because even though inflation has not yet reached the 2% target, a worsening employment situation could force the Fed to adjust its policy to support the economy and the labor market. A stable Core CPI at 3.1% and signs of economic weakness lead investors to believe that the Fed has few reasons left to delay easing. However, even with a 1% reduction, interest rates will still be in "restrictive" territory, so monetary policy overall is not yet considered to be strongly loose.

ECB Holds Rates Steady Amidst Inflation Concerns

The European Central Bank (ECB) decided to keep its deposit interest rate at 2%, in line with market expectations. This comes after the ECB had already implemented 8 key rate cuts over the past 12 months, starting in June 2024. Inflation in the euro area is now approaching the ECB's 2% target, with forecasts of 2.1% in 2025, 1.7% in 2026, and 1.9% in 2027. Core inflation (excluding food and energy) is projected to remain at 2.4% in 2024.

Meanwhile, the region's economic growth remains weak. Q2 GDP grew by only 0.1%, much lower than the 0.6% seen in Q1. The growth outlook has slightly improved, with forecasts of 1.2% in 2025 (up from 0.9% previously) and 1% in 2026. The ECB is signaling a temporary pause in rate cuts, but in the future, it may continue to ease policy and inject money to stimulate the economy, especially with many countries like France facing difficulties. However, this also carries the risk of inflation returning.

In reality, the inflation experienced by the public is higher than official figures, as seen in the sharp increase in the price of goods like food (e.g., the price of beef in the US increased from ~$49 in 2024 to ~$78 in 2025). Inflation and money-printing policies are causing asset prices to continue to rise, while incomes fail to keep up, which is widening the wealth gap.

Crypto Accumulation Trend and Market Updates

Global businesses continue to push forward with their crypto accumulation strategies. In Japan, ANAP just purchased an additional 29.58 BTC, raising its total holdings to 1,047.56 BTC. In Sweden, H100 Group added 21 BTC, bringing its total ownership to 1,025 BTC. Meanwhile, in the US, LIXTE Biotechnology initiated its digital asset treasury with 10.5 BTC and 300 ETH.

In parallel, the Avalanche Foundation is preparing to raise $1 billion to establish two crypto treasury companies, focused on purchasing millions of AVAX from its internal fund at a discounted price. The two main deals involve Hivemind Capital ($500 million through a Nasdaq-listed company) and Dragonfly Capital ($500 million through a SPAC). The long-term goal is to accumulate AVAX, similar to MicroStrategy's "Bitcoin treasury" strategy. The total supply of AVAX is capped at 720 million tokens, of which approximately 422 million are currently in circulation.

On the regulatory front, the Hong Kong Monetary Authority (HKMA) has just announced new draft guidance, proposing to relax capital requirements for banks holding certain crypto assets. Assets built on permissionless blockchains could be subject to lower capital requirements if they have appropriate risk governance mechanisms. This move aims to align Hong Kong's legal framework with Basel standards and is expected to officially take effect in early 2026.

Sources

- Bloomberg

- CoinDesk

- U.S. Treasury

- TradingView

- Reuters

- SEC

- White House Press Office

- CME FedWatch Tool

- Trueflation

- European Central Bank (ECB)

- Metaplanet Investor Relations

- ANAP Investor Relations

- H100 Group Investor Relations

- LIXTE Biotechnology Investor Relations

- Avalanche Foundation Official Announcements

- HKMA Official Announcements

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Please do your own research before making investment decisions.