Hyperliquid recently witnessed a fierce competition for the right to issue USDH, the ecosystem's first stablecoin. More than just a new stablecoin, USDH marks a major step forward for Stablecoin 2.0, a model that shares yield with the community.

The Billion-Dollar Bidding War on Hyperliquid: Competing for the Right to Issue USDH

Stablecoin 2.0 and Hyperliquid's USDH Tender

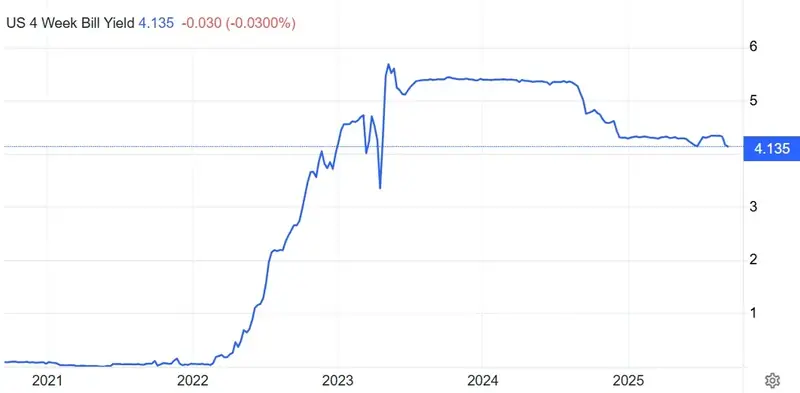

Stablecoin 2.0 represents a new evolution in stablecoin design, where the yield generated from reserve assets (primarily US government bonds) is returned to the community instead of being kept by the issuer. In a context where short-term US Treasury yields are over 4% annually, the tens of billions of dollars in reserves held by USDC or USDT generate hundreds of millions of dollars in profit.

Previously, this yield belonged entirely to the stablecoin issuer, while users received nothing. The Stablecoin 2.0 model was created to change this dynamic: it aims to be more transparent, share value, and directly align the interests of the issuer with the community.

The public tender for the right to issue USDH on Hyperliquid is a prime example of this. Instead of issuing the stablecoin themselves or choosing a partner behind closed doors, Hyperliquid forced organizations to compete with specific proposals, ranging from profit-sharing ratios to plans for ecosystem support. This move was designed to recapture a massive stream of yield that was previously flowing out of the ecosystem and bring it back to the platform.

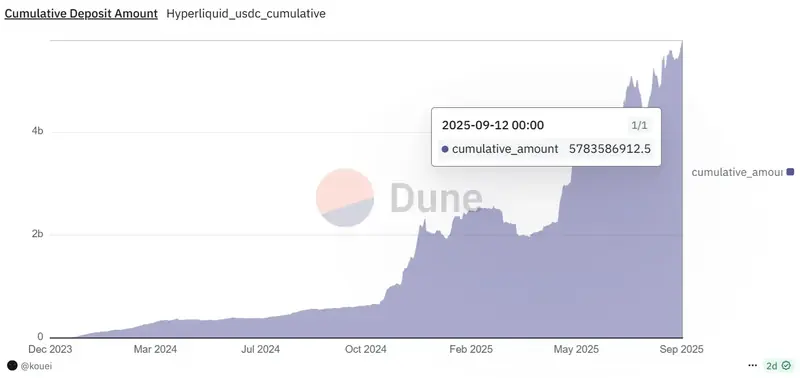

Currently, Hyperliquid holds approximately 5.7 billion USDC, which accounts for over 7% of the total global USDC supply. At current interest rates, these reserves could generate over $200 million in annual profit, a figure that previously belonged entirely to Circle (and its partner, Coinbase).

Crucially, the final decision was not made by a small group but was executed on-chain, through a vote by validators staking HYPE, requiring a two-thirds majority consensus. This marks a new era where the community becomes the "customer" that stablecoin issuers must try to win over. This is a fundamental shift in the balance of power, moving from a centralized model where yield flows to the issuing company, to a decentralized model where the benefits are returned to nurture the ecosystem itself.

Hyperliquid also set high standards for the proposals, requiring them to comply with regulatory frameworks like the GENIUS Act or MiCA, while also demanding integration of fiat on/off-ramps to make the stablecoin user-friendly. The yield from the reserve assets will be used to buy back HYPE, distribute it to the community, or transfer it to an ecosystem support fund, thereby directly increasing the value for HYPE holders.

Therefore, USDH is not just a new stablecoin for trading; it's a symbol of the Stablecoin 2.0 era, where issuers must compete to give the most value back to the community. This could be a pioneering model that many other ecosystems will adopt in the future.

Analysis of the Main Proposals: Paxos, Frax, Agora, and Native Markets

Paxos

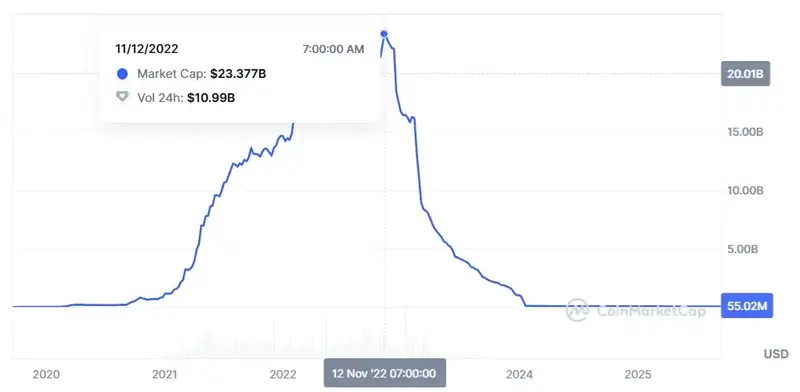

Paxos entered the race with the advantage of being a major player with years of experience in the stablecoin space. It not only issued BUSD, which reached a market cap of $23 billion, but it also powers PayPal's PYUSD, one of the fastest-growing stablecoins on the market.

With its proposal to issue USDH, Paxos chose to bring its entire regulatory compliance framework and traditional infrastructure to Hyperliquid. USDH would be issued directly on HyperEVM and HyperCore, primarily backed by US government bonds and cash, held in segregated custody, and regularly audited. In terms of technical and legal aspects, this was a safe, familiar, and proven solution.

Paxos's biggest highlight was its commitment to sharing yield. Initially, it promised to cede 95% of the yield from USDH reserves to the Hyperliquid ecosystem, but in response to community feedback, Paxos adjusted to a tiered model: in the initial phase, nearly 100% of the yield would go back to Hyperliquid, and only when TVL surpasses $5 billion would Paxos keep a maximum of 5%. Notably, 70% of the expected yield would be transferred to an on-chain Support Fund, with the rest distributed directly to HYPE. Paxos even added a "gift" of $20 million from PayPal to incentivize the ecosystem, treating it as a marketing and user-support budget to encourage the switch to USDH.

72 hours. Every comment read and concern addressed.

— Paxos (@Paxos) September 10, 2025

We’re out of the war room, with @PayPal + @Venmo on board.

USDH Proposal v2:

❏ PayPal ecosystem integrations + $20M incentives

❏ AF pledge starts at 20% and rises w/ TVL

❏ Paxos takes 0 until >$1B, capped at 5% past $5B pic.twitter.com/eLucHcw63h

In terms of on/off-ramps, Paxos is nearly unrivaled. It holds a NYDFS license, is prepared for MiCA compliance in Europe, is federally approved by the OCC, and has deep relationships with global financial institutions. From SWIFT to PayPal, Venmo, and Checkout, Paxos's payment network is powerful enough to take USDH beyond the confines of DeFi and turn it into a real-world payment tool. The mere prospect of PayPal users being able to buy HYPE or transfer USDH to each other for free would be a massive boost for Hyperliquid.

But this very "safety" and "compliance" were also perceived as a weakness by some in the community. Paxos, despite promising high profit-sharing, still reserves a maximum of 5%, whereas crypto-native teams like Frax were willing to return 100%. The incident where BUSD was forced to stop issuance by the NYDFS remains a lingering concern, reminding people that USDH could one day be halted due to political pressure. The ability to blacklist wallet addresses based on legal requests also made many DeFi investors wary. More importantly, Paxos is an "outsider." It entered as a large corporation, while the Hyperliquid community seemed to favor names that were more integrated and shared the "crypto-native" culture of the ecosystem.

Frax Finance

Frax Finance entered the USDH bidding war with the image of a "pioneering DeFi project" that had a completely different philosophy than Paxos. Instead of operating as a traditional issuer, Frax built a full alliance combining DeFi and TradFi: Frax handles the on-chain infrastructure, a federally regulated US bank manages the issuance and custody of fiat, and names like BlackRock, Fidelity, Superstate, and WisdomTree are behind the management of tokenized US government bonds. This is all integrated with LayerZero for cross-chain support, and Bridge/Stripe to handle legal compliance. The goal was to create a USDH that was both regulatory compliant and still retained the soul of DeFi.

What caught the community's attention most was the "0% revenue capture" commitment, meaning that all yield from the reserves (primarily US government bonds) would be returned to Hyperliquid, without Frax retaining any portion. The distribution of this yield would be entirely up to governance: it could be used to buy back HYPE, fund the Assistance Fund, reduce fees for traders, or even create a savings program for USDH depositors.

Technically, Frax is no stranger to the space. The team previously operated FRAX, an algorithmic stablecoin that once had a market cap of over $2 billion. They also have frxETH, FraxLend, and FraxSwap—all popular DeFi products, proving their ability to manage a peg, create liquidity, and expand an ecosystem. Their current alliance is even stronger, from BlackRock to Fidelity, all major RWA players. This combination made many believe that Frax was offering a "standardized DeFi version of USDH," backed by TradFi giants.

However, there were also drawbacks. Frax had not publicly named its partner federal bank. Relying on this "unknown" entity made many validators wary: what would happen if the bank withdrew? In fact, Frax received no support from any validators in the USDH bidding vote. Furthermore, Frax had never directly issued a regulatory-compliant stablecoin like Paxos, meaning it lacked experience in dealing with regulatory bodies. It also didn't have the massive on/off-ramp channels like PayPal or Venmo to guarantee mass adoption. And because Frax committed 100% of the yield to the community, it wouldn't retain any portion to reinvest or fund large-scale incentives, unlike Paxos, which had a ready-made support fund from PayPal.

Agora

Agora entered the USDH race with the image of a "pure TradFi player," bringing a full alliance of Wall Street heavyweights. It partnered with State Street (a custodial bank managing up to $49 trillion in assets), VanEck (an investment fund with over $130 billion), along with Cross River and Customers Bank to handle issuance and on/off-ramps. On the crypto front, Agora brought in Rain to manage payment cards and LayerZero for cross-chain bridging. With such an ecosystem of partners, they built the image of a highly secure USDH, managed like an institutional asset, but with enough technology to operate on a multi-chain basis from day one.

72 hours. Every comment read and concern addressed.

— Paxos (@Paxos) September 10, 2025

We’re out of the war room, with @PayPal + @Venmo on board.

USDH Proposal v2:

❏ PayPal ecosystem integrations + $20M incentives

❏ AF pledge starts at 20% and rises w/ TVL

❏ Paxos takes 0 until >$1B, capped at 5% past $5B pic.twitter.com/eLucHcw63h

USDH's reserves, according to Agora's proposal, were also "textbook": cash, short-term bonds, and overnight repos, all managed by VanEck and custodied by State Street. They also promised to provide real-time on-chain proof-of-reserve data via Chaos Labs. This put Agora's USDH on par with, or even surpassed Paxos, in terms of reserve reliability, as both the investment and custody portfolios were in the hands of major players familiar to institutional investors.

A key point was Agora's commitment to returning 100% of the net yield from reserves to the Hyperliquid community. All of the bond interest, after deducting operational costs, would be used to buy back HYPE or be injected into the protocol's support fund. In other words, HYPE holders would fully benefit from this cash flow, while Agora wouldn't keep a single dollar. They even promised to contribute $10 million to provide initial liquidity for USDH, and were willing to cover the conversion fees from USDC to USDH so that users would incur no costs during the launch phase.

From a regulatory standpoint, Agora also went very far. With Cross River Bank (a name that has partnered with Circle and Coinbase), Agora could ensure USDH's compliance with the GENIUS Act. This would allow users to easily mint or redeem USDH via bank transfers. However, Agora was still missing a key piece: a MiCA license in Europe. If it wanted USDH to expand into the EU, this would be a gap that needed to be filled.

Still, Agora's meticulousness was also its weakness. It focused almost entirely on its TradFi machinery but showed little specific planning for integrating with Hyperliquid beyond sharing yield. There were no promises of deep integration with HyperEVM, no new DeFi ideas, or unique incentives for traders.

For a community accustomed to the vibrancy of crypto-natives, this approach could be seen as cold and distant. Furthermore, the current size of its AUSD stablecoin was only a little over $100 million, far too small compared to the expected $5-6 billion market cap that USDH could command. This made many wonder: was Agora truly ready to operate at such a massive scale? Similar to Frax, the Agora team received no support from any validators in the USDH bid.

Native Markets

Native Markets entered the USDH race with the posture of an "in-house team," born to serve Hyperliquid and only Hyperliquid. They were the only team to test a USDH contract directly on HyperEVM, and they submitted their proposal just over an hour after the vote was announced. This showed they had been preparing very early, almost waiting to become the official stablecoin issuer. Not only were they ambitious, but Native Markets also presented core infrastructure called CoreRouter, which was audited and open-source, proving they weren't just making promises but had already started building.

Unlike their rivals who chose indirect routes, Native chose a direct path to connect with the giants: USDH's reserves would be managed off-chain by BlackRock, while Superstate would handle the on-chain tokenization of US government bonds, all coordinated by Bridge (a platform that Stripe acquired in 2022). Thanks to this, even as a new name, Native Markets could leverage the immense reputation and infrastructure of Stripe and BlackRock to ensure safety, transparency, and regulatory compliance.

Native's profit-sharing strategy also reflected a clear long-term direction. It chose not to funnel all the yield into buybacks like Frax or Agora, but to allocate 50% to HYPE through a Support Fund and 50% for ecosystem development reinvestment. This means HYPE holders would directly benefit from the buyback cash flow, while the Hyperliquid ecosystem would also be nourished by a sustainable capital source—from funding builders and expanding the HIP-3 market to incentivizing new dApps on HyperEVM.

In the legal and on/off-ramp space, Native relies on Bridge (i.e., Stripe) to handle operations. Stripe already holds an MSB license in the US and has a global payment infrastructure, so USDH under the Native Markets proposal could easily be deposited/withdrawn with fiat, and even be integrated with credit cards and direct payment gateways. In theory, this is a superior advantage because if Stripe opens its doors, USDH could connect with millions of merchants worldwide. But at the same time, this is a double-edged sword: Stripe is developing its own blockchain called Temple, and many people worry that Bridge might prioritize its internal project over Hyperliquid.

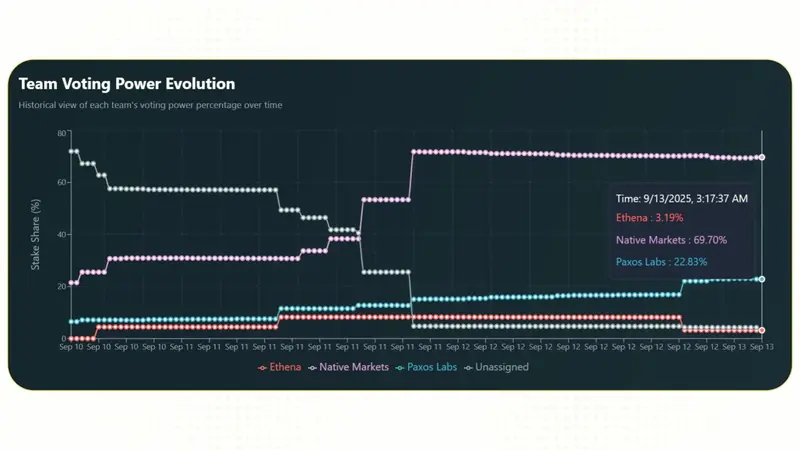

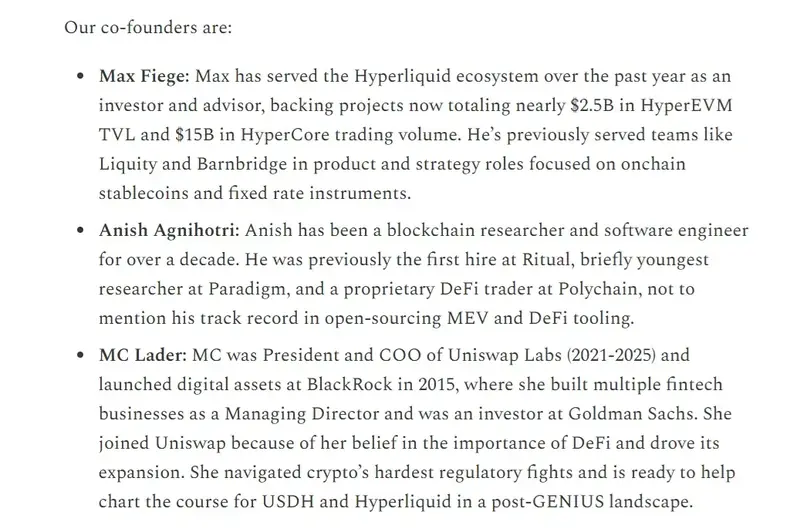

The biggest strength of Native Markets lies not in its infrastructure or legal standing, but in its deep connection to the Hyperliquid community. Their team consists of familiar faces, including Max Fiege—an early investor in Hyperliquid, MC Lader—former COO of Uniswap Labs, and Anish Agnihotri—a former Paradigm researcher. They are seen as "insiders" who truly understand the community's needs and culture. This is why Native Markets received strong backing from many validators, even leading a potential competitor, Ethena, to withdraw its bid to support them. With Native Markets, Hyperliquid has a team that is fully dedicated to USDH, rather than just viewing it as a side project in their portfolio.

The last few days have been incredible to witness. I've never seen a community rally around and engage with passion like this before.

— G | Ethena (@gdog97_) September 11, 2025

Following direct discussions with individuals in the community and validators we have taken onboard some of the concerns, namely:

-Ethena is not…

Still, Native Markets is not without questions. The team has never directly issued a stablecoin before, so no one can be certain they can pull it off. Its dependence on Bridge/Stripe is both a strength and a risk. If Stripe changes its strategy or encounters issues, USDH would be directly affected. Furthermore, their rapid appearance in the voting process made some people suspicious of whether the process was biased, even though major validators denied it. Finally, compared to Paxos with its experience operating billions of dollars in stablecoins or Frax with its vibrant DeFi community, Native is still a new name. To succeed, the team needs to prove its ability to operate at a massive scale, not just rely on its "community goodwill" advantage.

The Bidding Results

The official voting took place in just one hour (from 10:00 - 11:00 UTC on September 14, 2025), preceded by a 3-day early voting phase based on validator commitments. Native Markets officially won the bid with 68.87% of the total voting power, meeting the two-thirds consensus standard.

With Native Markets winning, the decision to allocate only 50% of the yield to HYPE means the direct financial income for holders is less than what was promised by other options. However, if the 50% of yield that is reinvested truly generates a significant amount of growth, the value HYPE receives could be much greater than the 50% of yield it gave up. Regardless of who won the bid, Circle and Coinbase are the biggest losers because the over $5 billion in USDC deposited on Hyperliquid will now be gradually replaced by USDH.

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Please do your own research before making investment decisions.