After consistently facing internal and external challenges, MakerDAO has completely redefined itself with Sky. This in-depth analysis will explore the motivations behind this radical transformation and what it means for the future of the ecosystem.

MakerDAO Before Sky: The Inevitable Transition

For nearly a decade, MakerDAO stood as a pioneering icon of decentralized finance (DeFi). The project was built on a core philosophy: to create a decentralized, transparent stablecoin independent of the traditional banking system. This stablecoin was DAI.

MakerDAO's mechanism was based on an overcollateralized lending model. Users could lock crypto assets like ETH, wBTC, stETH, etc., into "Vaults" to mint DAI, with a collateral ratio typically ranging from 130-175% to ensure system security. When the asset value plummeted, an automatic liquidation mechanism would activate: the collateral was auctioned off, and a portion of the proceeds, along with a fee, was used to repay the DAI debt. This system helped DAI maintain its 1:1 peg with the US dollar even during periods of high market volatility.

MakerDAO's revenue primarily came from three sources:

- Stability Fee: An annual borrowing fee (1-4%) used to buy and burn the MKR token, creating a deflationary mechanism and indirectly increasing value for MKR holders.

- Liquidation Penalty: A penalty of approximately 13% applied when a Vault was liquidated, contributing additional revenue to the system during volatile market conditions.

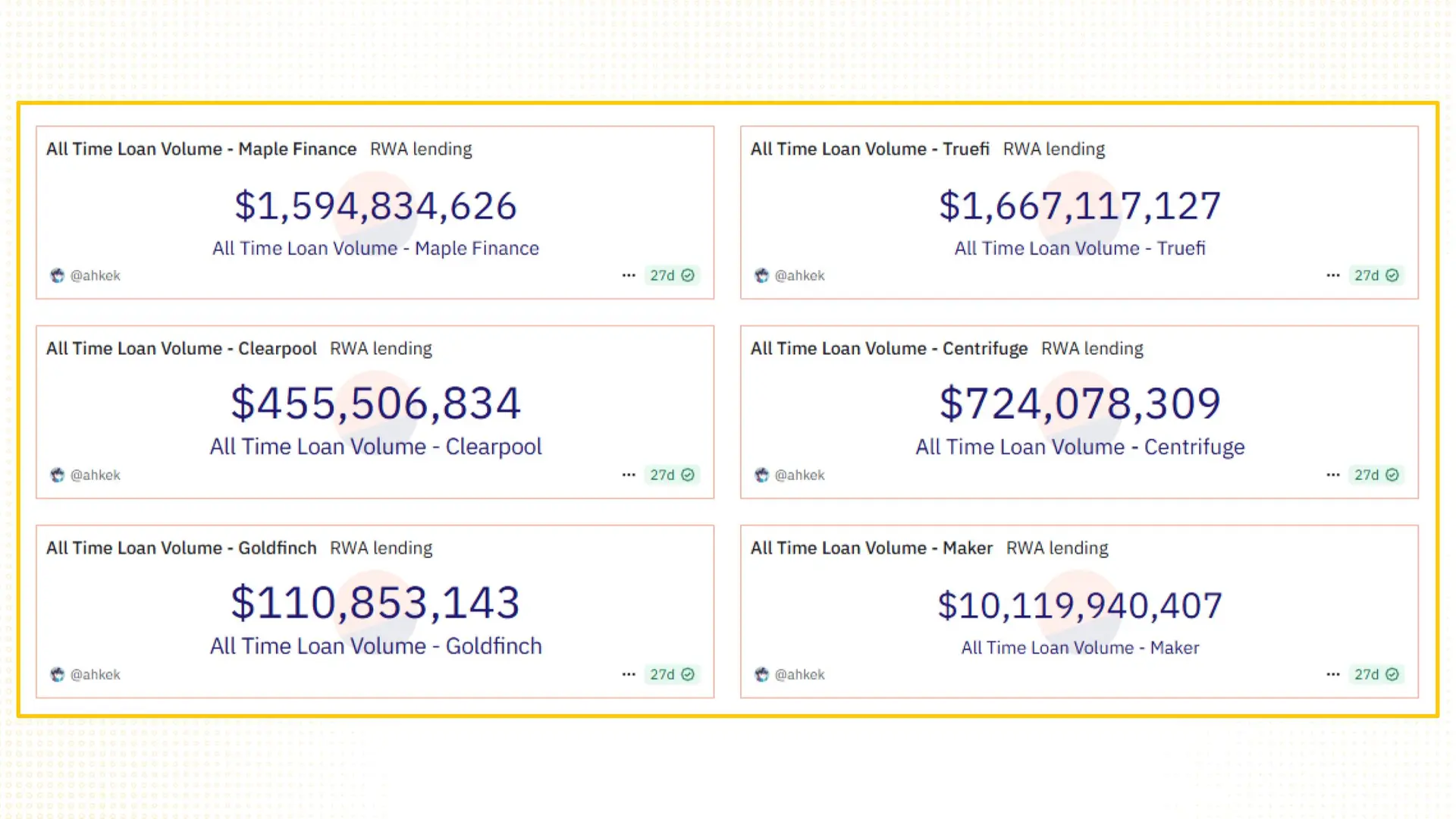

- Real-World Assets (RWA): Recognizing that complete reliance on crypto assets made the system vulnerable to price fluctuations, MakerDAO began a strategy in 2021 to expand into real-world assets. Through partners like Monetalis (backed by Rune Christensen himself), BlockTower, and Huntingdon Valley Bank, MakerDAO provided capital to traditional financial institutions to earn yield from US government bonds, commercial mortgages, and corporate loans. By mid-2023, over 50% of MakerDAO's collateral was in RWA, amounting to $2.5 billion, generating tens of millions of dollars in annual revenue. This made MakerDAO a leader in RWA loans with over $10 billion, far surpassing competitors like Maple Finance, Centrifuge, and TrueFi.

This strategy helped MakerDAO reach its peak during the 2021 uptrend, entering the top 3 DeFi projects by TVL and becoming one of the first true "DeFi Central Banks." However, along with the market's growth, several limitations began to emerge:

Internal Weaknesses within the Ecosystem

- Limited Scalability: The requirement for on-chain collateral to mint DAI meant that the supply expansion rate was much slower compared to centralized stablecoins like USDT or USDC, which can be issued quickly without collateral binding. During hot growth periods, demand for stablecoins surged, but MakerDAO couldn't scale fast enough, leading to a loss of market share to centralized rivals.

- Dependence on Centralized Assets: To ensure stability and yield in a fiercely competitive environment, MakerDAO accumulated a large amount of USDC and US government bonds. This was a rational strategy to reduce volatility and optimize capital efficiency but also made the system dependent on centralized entities and exposed it to legal risks, such as the potential for USDC to be frozen or for regulatory intervention.

- Ineffective DAO Governance: MakerDAO's governance mechanism, based on the MKR token, allowed holders to vote on critical parameters like collateral ratios, interest rates, and RWA strategy. However, the actual number of participants in voting was very low, with power concentrated in a small group of whales and the core team. This made MakerDAO slow to react to rapid market changes, reducing the diversity and decentralization of strategic decision-making.

- Unattractive MKR Value Mechanism: The MKR token primarily served a governance role without providing a direct cash flow to investors. The buyback & burn mechanism was weak because net profits were not high enough to be triggered frequently. Meanwhile, new-generation DeFi protocols like GMX, Lido, and Ethena began directly sharing revenue with stakers, making the MKR token less attractive from an investment perspective. As a result, despite reaching a peak of $6,000/MKR in 2021, MKR's market value did not increase commensurately with TVL and revenue, its liquidity weakened, and token distribution was low.

Pressure from the Global Stablecoin Market

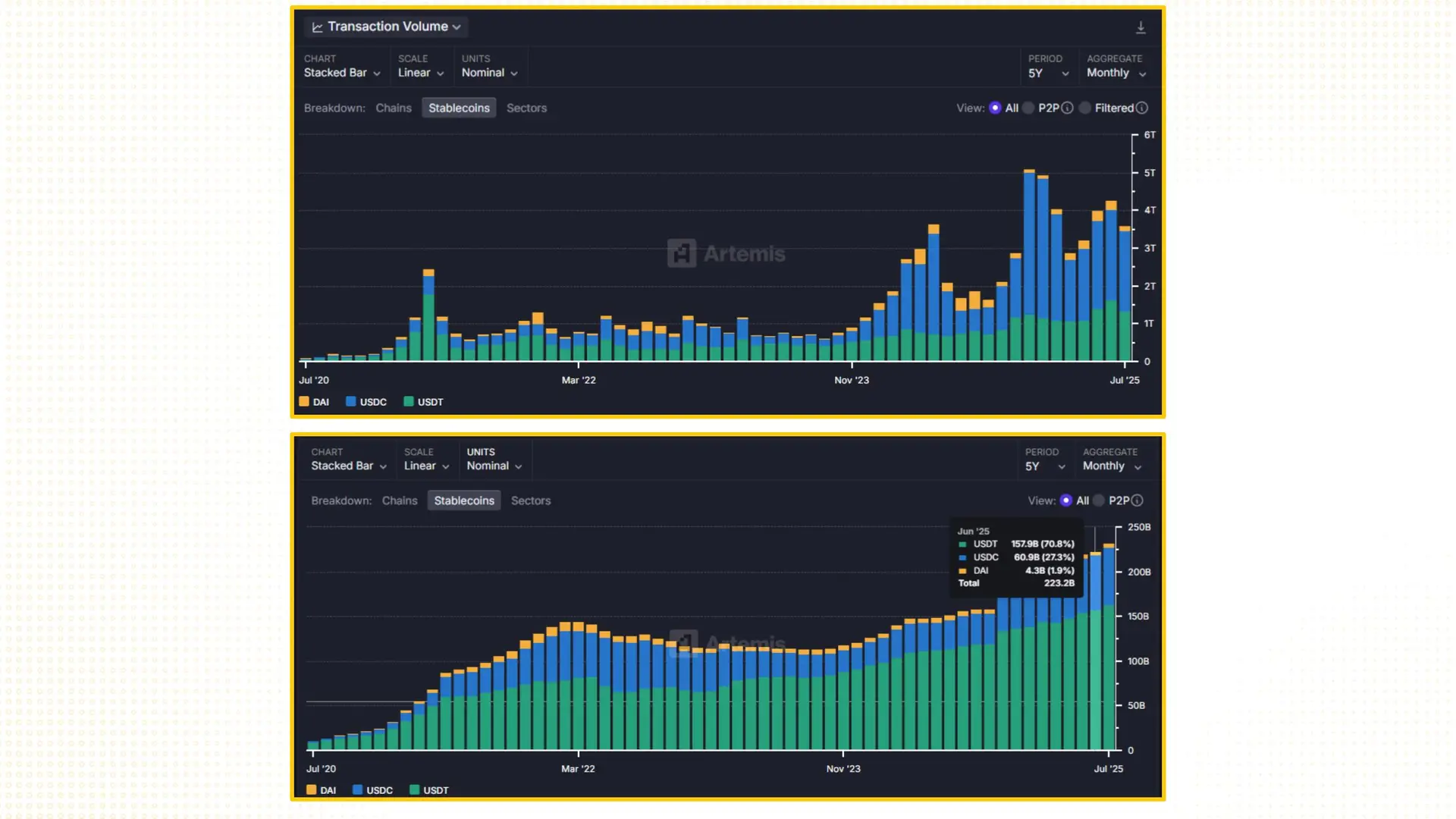

From late 2023 to mid-2025, the stablecoin market became increasingly unfavorable for DAI. The two giants, USDT (Tether) and USDC (Circle), accounted for over 90% of the total global stablecoin transaction value. They were not only the dominant payment methods in the cryptocurrency ecosystem but were also integrated by default into traditional financial applications and global payment platforms like Stripe, PayPal, and Shopify, as well as popular wallets like MetaMask and Coinbase Wallet.

In contrast, DAI gradually lost its foothold:

- Daily trading volume only fluctuated between $150-200 million, while USDT and USDC processed trillions of dollars monthly.

- DAI's total supply reached just over $4 billion by mid-2025, while USDT hit $160 billion and USDC neared $65 billion.

- DAI was almost absent from crucial Web3 payment applications like blockchain games, NFTs, decentralized social media, and Web3 e-commerce.

This lack of integration created a vicious cycle: low DAI usage led to low demand, which in turn meant developers didn't prioritize its integration. This decentralized stablecoin was gradually sidelined from real-world use cases, despite its superior transparency and decentralization.

The Restructuring Turning Point: The Origin of Sky

Faced with declining market share and persistent internal limitations, MakerDAO confronted a critical challenge for its survival: if it didn't change, the project would fall behind in the global stablecoin race. Rune Christensen, the founder of MakerDAO, realized that the problem could not be solved with minor tweaks to the existing model. Instead, a complete restructuring was needed to thoroughly address the bottlenecks in incentives, scalability, and long-term sustainability.

In mid-2023, Christensen officially initiated the Endgame Plan, laying the groundwork for the transformation of MakerDAO into Sky—a multi-layered, modular ecosystem where the stablecoin, governance token, and SubDAOs were redesigned. The goal of the Endgame Plan was not just to restore the position of a decentralized stablecoin but also to build a DeFi model strong enough to survive and thrive for decades to come.

From MakerDAO to Sky: An Ecosystem Overhaul

The biggest difference between MakerDAO and Sky lies in their governance structure. In the old model, all activities were decided centrally within a single DAO. This approach caused delays and a lack of flexibility as the system had to handle too many different areas.

Sky addresses this by implementing SubDAOs: independent operational units, with each SubDAO focusing on a specific function such as lending, liquidity management, RWA, or treasury, but all operating under a unified governance framework coordinated by the SKY token. Concurrently, DAI was upgraded and renamed USDS. USDS serves as the common operational core, connecting the SubDAOs and providing liquidity to the entire ecosystem, thereby increasing capital efficiency and scalability compared to the old model. Additionally, the ecosystem introduces the Sky Stars system: satellite products or protocols revolving around USDS, deployed as experiments for a new generation of decentralized governance models. This is a crucial step, helping Sky maintain innovation flexibility while ensuring order and a unified strategic direction for the entire system.

USDS: Sky's New Stable Foundation

As mentioned, DAI was heavily influenced by USDC, with over 50% of its collateral at one point coming from wrapped USDC via the Peg Stability Module (PSM) mechanism. This limited DAI's scalability and raised concerns about its true decentralization. The USDS stablecoin was redesigned to thoroughly solve this problem, with the goals of:

- Expanding the collateral base through RWA protocols, reducing dependence on centralized stablecoins.

- Optimizing capital efficiency, improving liquidity, and enabling integration with global payment systems.

Technically, USDS maintains its 1:1 peg with the USD but is supplemented with new tools to increase utility and peg stability:

- Peg Stability Modules (PSM): Allows users to swap USDS with other stablecoins (USDC, USDT) with minimal spread, maintaining stability and liquidity even under volatile market conditions.

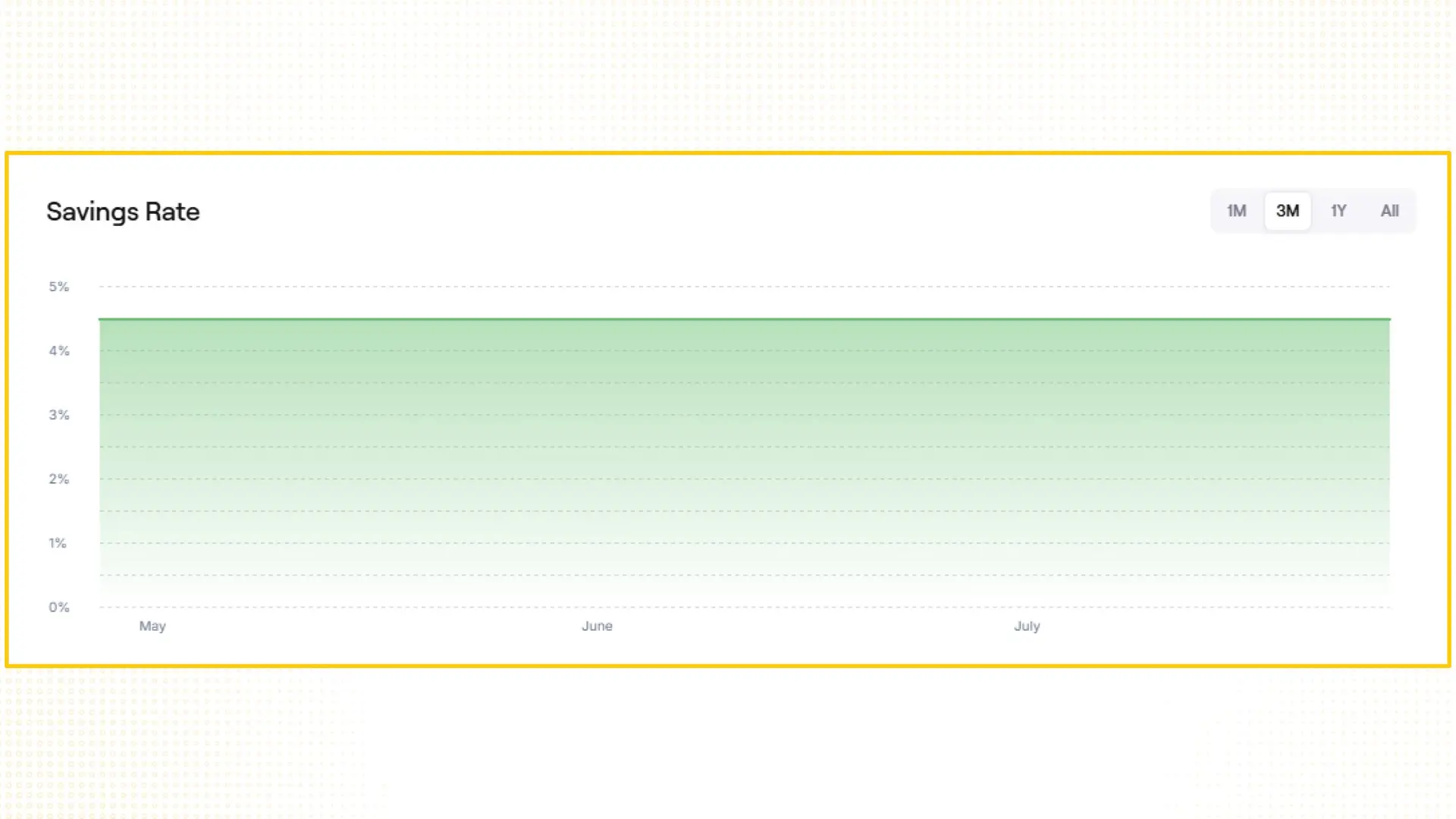

- Sky Savings Rate (SSR): An upgraded version of the previous Dai Savings Rate (DSR). If the DSR allowed staking DAI to earn interest but had limitations on fees and capital reusability, SSR fixes this by automatically issuing sUSDS, allowing users to both earn an approximate 4.5% APY interest and easily participate in other ecosystem activities.

- Sky Token Rewards (STR): Incentivizes users to stake USDS to receive rewards in SKY tokens, creating internal demand for the stablecoin and promoting a circulating flow of capital within the ecosystem.

- Collateral Utility: Notably, USDS is designed to become the core collateral asset in the Sky ecosystem's flagship products, most prominently Spark Protocol, a SubDAO dedicated to lending. This creates a seamless connection between the stablecoin, lending activities, and governance across the entire Sky ecosystem.

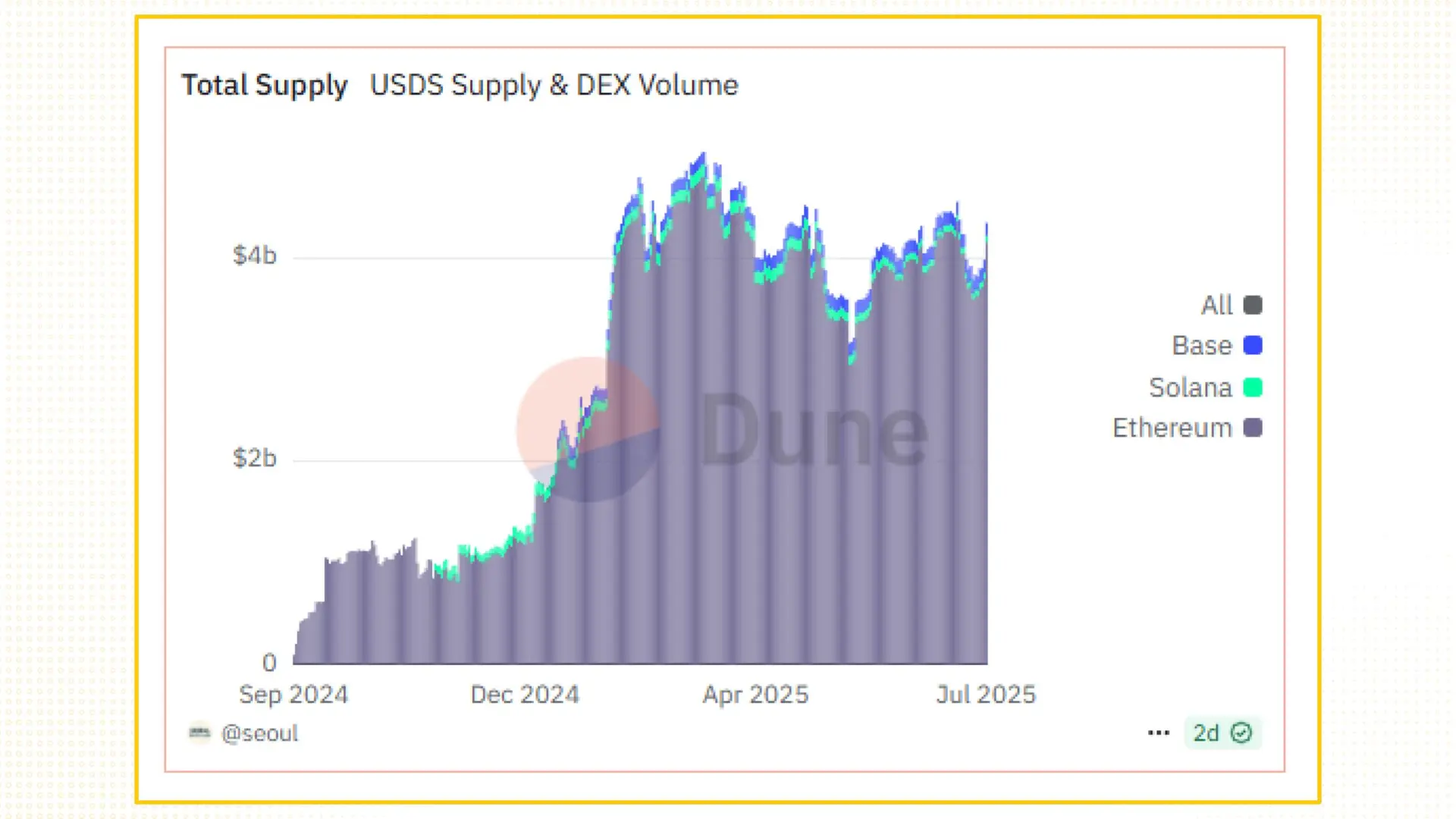

In addition to feature upgrades, USDS also changes its business model. Instead of all profits flowing to the governance token as before, Sky implements a USDS Revenue Share mechanism, allocating a portion of the profits from SubDAOs directly to USDS holders through reduced fees or internal rewards. This approach helps build user loyalty, transforming USDS from a mere payment tool into an integral part of Sky's incentivized economy. Currently, USDS has reached a TVL of over $4.3 billion on Ethereum, with daily trading volume maintaining around $1-3 billion and over 50,000 daily transactions.

The SKY Token: From Voting Power to Long-Term Economic Pillar

The conversion from MKR to SKY at a 1 MKR : 24,000 SKY ratio is a crucial part of the Endgame Plan. This change is not only aimed at reducing the unit price to make the token more accessible to retail investors and more convenient for incentive programs, but also at completely redefining the token's role within the ecosystem.

In the old model, MKR primarily served a governance function. Its high price made it inaccessible to most users and provided little incentive for them to participate in staking or voting. Furthermore, this token did not generate direct cash flow for investors, and the buyback & burn mechanism was inconsistent due to low net profits, making MKR lack long-term appeal.

With SKY, the mechanism is redesigned to transform the token from a mere voting tool into a genuine economic pillar. Users can stake SKY into SubDAOs to earn direct profits from each unit's business operations. For example, staking into the Spark SubDAO helps earn a portion of the profits from lending activities, while staking into the Atlas SubDAO generates fees from RWA strategies. This approach creates a closed economic loop: stake SKY → provide capital or insurance → earn yield → continue to hold SKY, thereby strengthening the token's value over time.

To maintain sustainable value, Sky implements a buyback and lockstake mechanism:

- Manual Buyback: Conducted periodically or during special events, using profits from SubDAOs to buy back SKY from the market.

- Auto Buyback Auction: An automatic mechanism for auctioning buybacks of SKY, ensuring transparent transactions and avoiding abnormal price volatility.

- Lockstake: Incentivizes users to lock SKY for long periods (6-36 months) to receive additional rewards from SubDAO activities and the redistributed amount of repurchased SKY.

This mechanism offers two main benefits: it reduces selling pressure as users who have locked their SKY for the long term are less likely to panic sell, helping the price remain stable. It also creates a scarcity effect: the more SKY is locked, the lower the circulating supply becomes, making the price more likely to increase as demand for staking and buybacks remains steady.

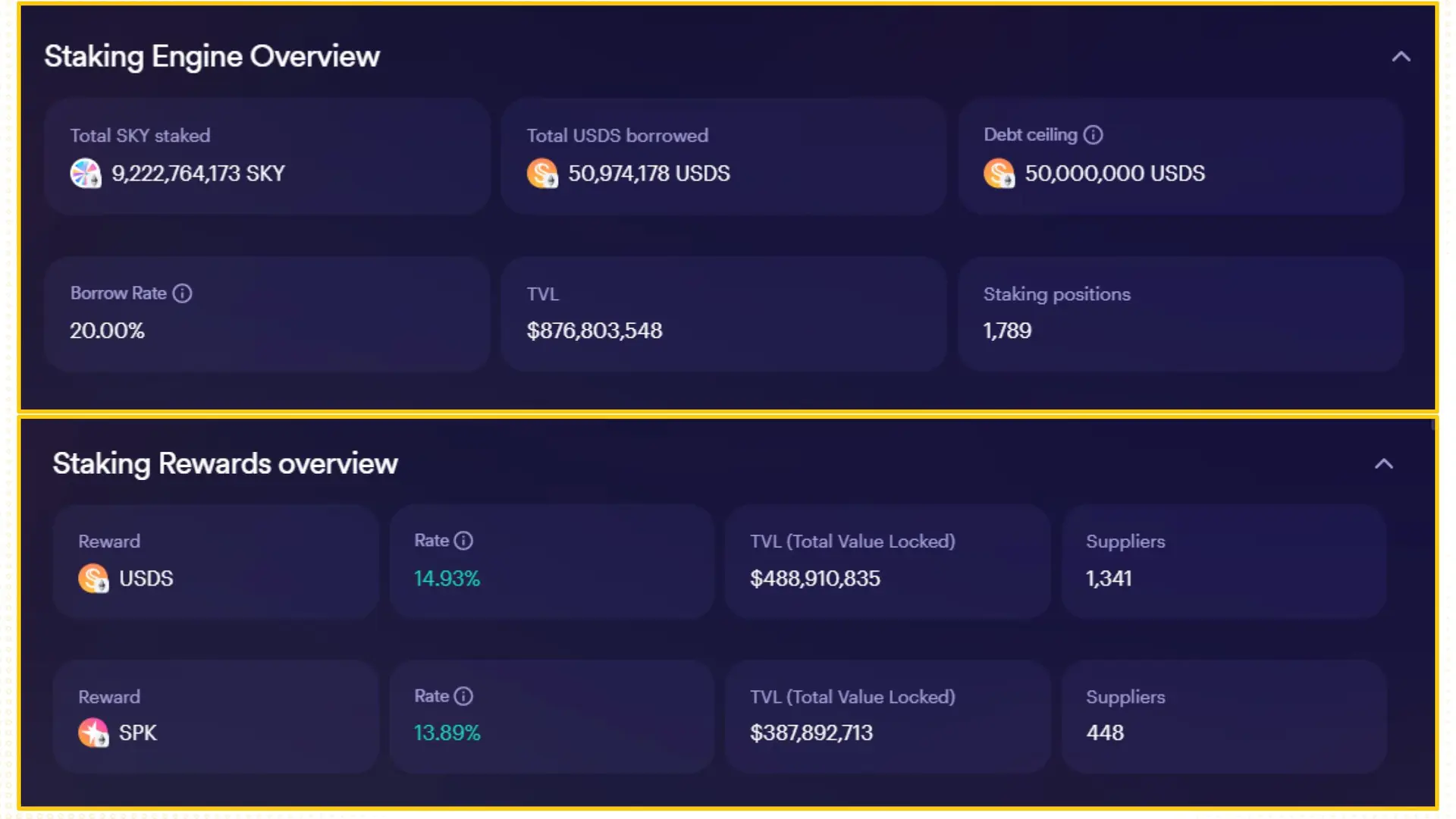

Thanks to these mechanisms, the Sky ecosystem has recorded over 9.2 billion SKY staked, equivalent to approximately $875 million, which accounts for over 43% of the total circulating supply. Currently, the circulating market cap of SKY is only about $1.5 billion, nearly 4 times lower than the TVL of nearly $6 billion, indicating a high level of accumulation and token locking. Furthermore, the staking rewards pool for SKY holders has reached a TVL of $400 million, with a Staking Reward Rate (SRR) fluctuating around 13-15%. With this yield level, SKY becomes a noteworthy choice for investors seeking a stable strategy, while also increasing the incentive to accumulate and hold the token for the long term.

The MKR to SKY Conversion Roadmap: A 'Nudging' Mechanism to Mitigate Market Shock

However, when converting from the MKR token to SKY, MakerDAO's biggest challenge was not the conversion rate between MKR and SKY, but how to avoid the liquidity shock and selling pressure typically seen when a new token is launched.

To address this, MakerDAO implemented a behavioral mechanism called the Delayed Upgrade Penalty (DUP): a "nudging" strategy that spreads the conversion process over time, allowing the market to absorb the change better and avoid abnormal price volatility. According to the design:

- From now until September 18, 2025, holders can convert MKR to SKY at the original 1:24,000 ratio without penalty.

- After this date, the conversion rate will decrease by 1% every 3 months, and the penalty will gradually increase until it reaches 100% after 25 years.

The portion of SKY not claimed by late upgraders will be held in a Converter Contract, under the governance of the Sky Ecosystem Governance, which opens up two possibilities:

- It can be re-allocated to the community through ecosystem development programs, staking rewards, or support for new SubDAOs.

- It can be completely burned, depending on the community's decision.

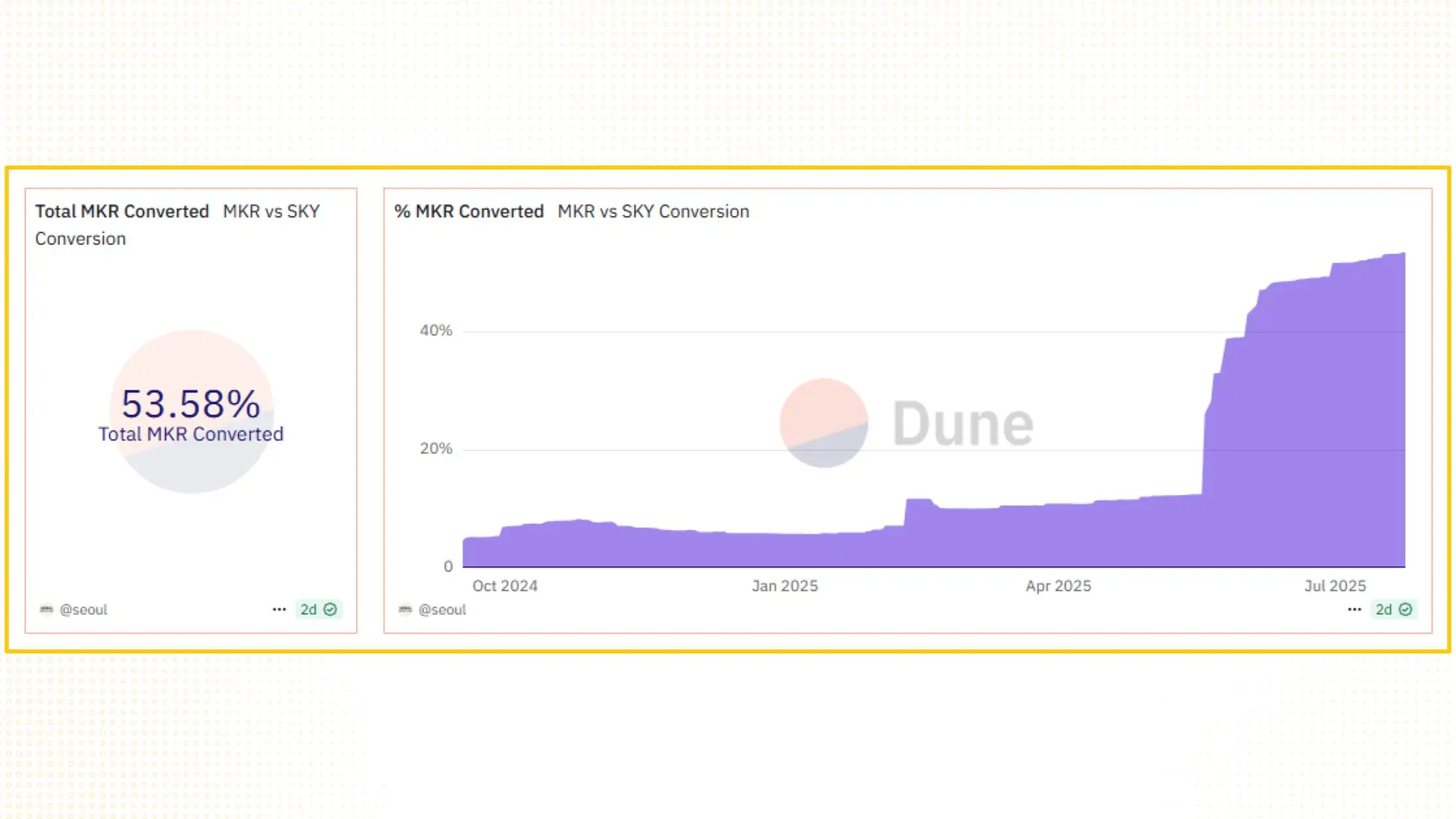

This approach ensures that the unallocated SKY does not become a source of selling pressure, while creating an incentive for the community to act early. To date, over 53% of the total MKR supply has been converted to SKY, showing high consensus and positive momentum for the prices of both tokens. When the first penalty thresholds are activated, SKY's price may continue to react positively due to a gradually decreasing circulating supply.

However, the DUP mechanism is only the beginning. The next factor to shape Sky's long-term value will come from its SubDAO ecosystem, centered around the Spark Protocol and the "Sky Stars" operational model.

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Please do your own research before making investment decisions.