On October 11th, the crypto market witnessed one of its fastest collapses in history, with over $19 billion in leveraged positions wiped out. Was this an unpredictable "Black Swan" event, or a foreseeable outcome of excessive leverage?

The Anatomy of the $19 Billion Liquidation

The morning of October 11, 2025, saw one of the fastest price drops in crypto market history. In just a few hours, over $300 billion vanished from the crypto market capitalization. Bitcoin, Ethereum, and Solana plummeted simultaneously, blowing out millions of leveraged positions. This date has become another "white night" for investors.

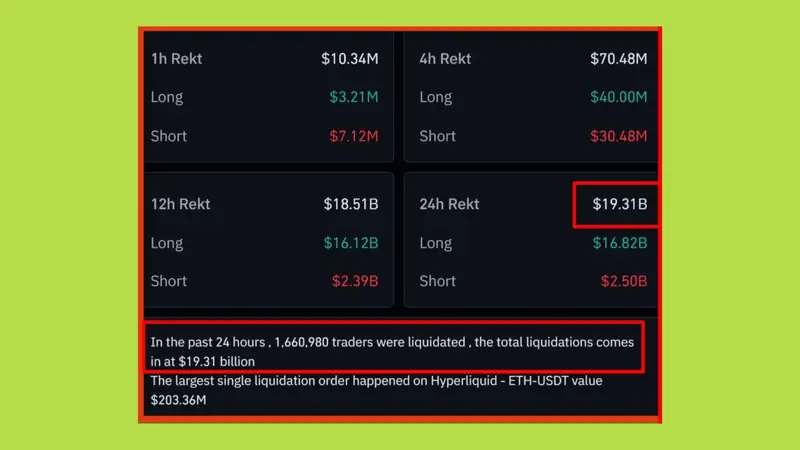

According to CoinGlass, the total value of liquidated positions exceeded $19 billion, a figure sixteen times higher than the collapse during the COVID-19 shock of 2020 and twelve times higher than the FTX event in 2022. On exchanges alone, Binance recorded $2.4 billion in liquidations, while the Hyperliquid DEX reached over $10 billion, demonstrating the widespread volatility across both centralized and decentralized markets.

However, according to Jeff, the founder of Hyperliquid, the liquidation figures from individual exchanges might not fully reflect the reality. He noted that Hyperliquid's on-chain liquidation mechanism is fundamentally different from CEXs, where data display is often limited or slow to update.

In addition to the liquidated assets, CoinGlass data shows that over 1.6 million accounts were liquidated. Furthermore, several major exchanges reported system failures, preventing users from accessing or closing their positions.

Naturally, as the market descended into chaos, numerous theories immediately emerged. Many attributed the crash to President Donald Trump's announcement that he would unexpectedly impose 100% tariffs on Chinese goods and tighten export controls on US "strategic" software. The US stock market, not just crypto, also saw a $2 trillion loss in market capitalization immediately following Trump's statement. On social media platforms, the term "Black Swan" quickly spread, serving as an immediate explanation for the unimaginable collapse.

But was the October 11th crash truly a "Black Swan" event, or was it a predictable consequence of a market strained to its limits by leverage?

"Black Swan": A Misused Concept for Market Crashes

According to philosopher Nassim Nicholas Taleb, a "Black Swan" event combines three criteria: (1) It is unpredictable before it occurs; (2) It has a massive impact and changes the systemic order; (3) After it happens, people tend to rationalize it, claiming "it was obvious all along." This concept was designed to describe shocks that lie outside the scope of prediction—catastrophes that originate from a risk zone that no statistical model or historical data can cover.

However, in real-world financial markets, the term "Black Swan" is often misused as a justification. When suffering losses, investors tend to blame the market's "surprise," rather than acknowledging that most collapses show early signs.

Market Structure Before the Crash: The Fuel Was Ready

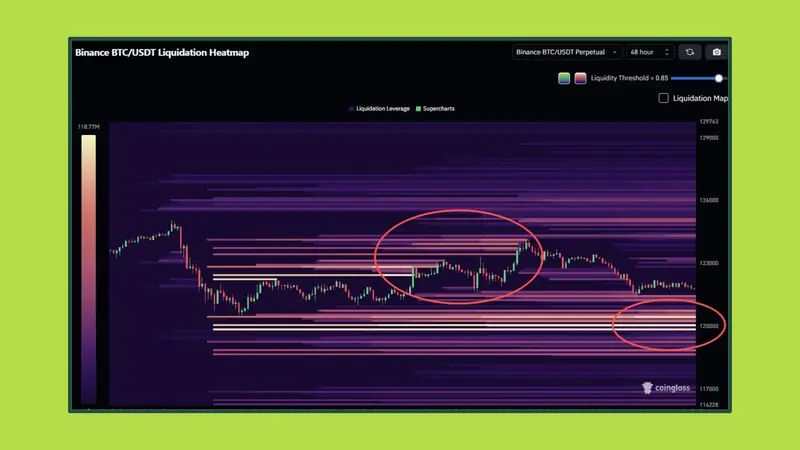

According to data from Coinglass and Glassnode, the total open interest (OI) reached over $120 billion, with nearly 87% in long positions. This severe imbalance indicated excessive optimism. Many investors were using leverage of 50x–100x, betting that the Bitcoin price would continue to surge past $150,000 in Q4.

This story wasn't limited to Bitcoin. ETH's open interest grew from $23 billion at the start of the year to nearly $60 billion just before the crash—an increase of nearly 160%. For Solana, the figure was even higher: a 205% surge in just the first nine months of the year. According to Glassnode, the parallel increase in price and open interest showed that leveraged capital was piling onto the upward trend, making the market structure extremely fragile.

High leverage means that only one strong enough macro shock is needed to trigger a cascading liquidation chain across the entire system. On October 10th, China announced tighter export controls on rare earth elements, critical materials for chip and crypto mining equipment. Observers immediately warned of potential US tariff retaliation, raising fears of a new trade spiral. However, the "Uptober" sentiment seemingly caused the community to ignore this warning.

With leverage at historically high levels, liquidity concentrated among a few large market makers, and an unstable macro backdrop, the market was a powder keg waiting for a spark. When Trump announced the 100% tariff on Chinese goods, the spark was lit at the perfect moment, turning the entire leveraged structure into an unstoppable chain reaction.

If we check Taleb's three criteria, the October 11th crash only meets two: massive impact and post-facto rationalization. The most crucial criterion—unpredictability—is not truly met. Signals of risk, from record leverage, severe directional bias, thin liquidity, to political risk, were visible weeks before. While no one knew the exact timing, the direction of the risk was completely predictable. Therefore, calling this crash a "Black Swan" is inaccurate. The correct term is "Gray Rhino": a large, obvious risk that is ignored until it charges.

Was the Crash Caused by Exchanges? The On-Chain Perspective

Immediately after the crash, not only did asset prices plummet, but community trust also eroded. On X and various forums, numerous posts spread accusations that Binance and other large exchanges had "ignited" the mass liquidation to profit from funding fees and forced closures. Suspicion was further heightened when a series of tokens listed on Binance, such as ATOM, recorded abnormal volatility, being "wiped" nearly 99.9%, dropping from $4,000 to $0.01 in minutes. Many low-leverage investors also had their accounts liquidated, making Binance the first target of public outcry. At the same time, some traders reported being unable to close positions due to "system overload" errors, while internal market-making accounts allegedly operated normally.

Binance initially maintained that its Futures, Spot, and API systems were "stable," but later admitted to internal oracle errors and a depeg phenomenon with assets like USDE, BNSOL, and WBETH. However, on-chain data suggests otherwise. According to MetaFinancialAI, Binance's hot and cold wallets recorded no unusual outflows during the volatility. Wallets confirmed to belong to CZ also showed no selling activity, and most of the exchange's cold wallets remained "dormant" for months. This indicates no clear evidence of Binance actively manipulating or "dumping" assets. In fact, after the incident, the exchange compensated affected users over $283 million within 24 hours, an action demonstrating responsibility rather than profiteering intent.

Due to significant market fluctuations over the past 16 hours and a substantial influx of users, some users have encountered issues with their transactions. I deeply apologize for this. If you have incurred losses attributable to Binance, please contact our customer service to… https://t.co/9Q7GZuFY5H

— Yi He (@heyibinance) October 11, 2025

As soon as the on-chain data confirmed this, community attention immediately shifted to Coinbase and Wintermute—two major links in the global liquidity network. Just before the crash, Coinbase transferred about 1,066 BTC from a cold wallet to a hot wallet, an action usually associated with preparation for large-scale trading. Simultaneously, a new wallet (believed to belong to a US institution) purchased about 1,100 BTC from Binance and transferred it to Coinbase just days before the price drop. In parallel, market maker Wintermute was heavily involved in asset transfers between exchanges. Data shows that the circulating assets between Binance, Wintermute, and Coinbase recently reached tens of billions of dollars. When these major players simultaneously withdraw orders, secure capital, or rebalance portfolios, the market's order book depth collapses, causing prices to fall vertically in minutes.

The October 11th Crash: A Painful Lesson in Market Maturity

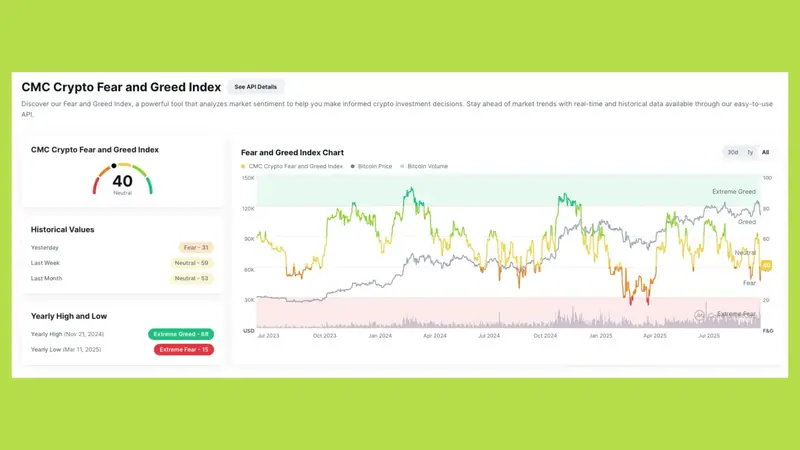

The events of October 11th led many to believe that the market was about to enter a "downtrend." But just two days later, the picture looked vastly different. According to data from EGA Crypto, over $220 billion in capital flowed back into the market, and the total industry market capitalization recovered from $2.9 trillion to over $3.1 trillion. Bitcoin rose from $110,000 to $115,000, and the Fear & Greed Index, which had plummeted to 27 (extreme fear), returned to the neutral zone.

The rapid recovery was driven not only by technical buying but also by cooling macro signals. Just one day after causing shockwaves with his 100% tariff announcement on China, Donald Trump surprisingly changed his tune: "Don't worry about China, everything will be fine... America wants to help, not hurt." This statement brought global relief. US stock indices uniformly rebounded, and risk appetite quickly returned. This provided the catalyst for capital to flow back into crypto after fear had been amplified to the extreme.

From a psychological perspective, the October 11th crash was a necessary wake-up call. After the initial "Uptober" excitement, the market was forced to confront reality: leverage is a double-edged sword. When the market is driven by news and sentiment, high leverage means investors no longer control their portfolios. Moving forward, risk management must be the top priority. Limiting margin ratios, placing stop-loss orders, and not leaving all assets on a single exchange are basic principles that many ignore until it's too late. Finally, choosing transparent and secure trading platforms is essential. The recent crash showed that a single system error or concentrated liquidity can send the entire market into a freefall within minutes. Allocating assets appropriately across CEXs, cold wallets, and spot products significantly reduces risk.

Ultimately, maintain a long-term vision. Short-term volatility does not reflect the whole picture. Institutional capital remains committed, and sharp corrections are sometimes the very opportunities needed to accumulate assets at reasonable prices. For those with enough patience, the market "learning to endure pain" is when investors have the chance to become more resilient.

Sources:

- CoinGlass (Liquidation Data, F&G Index)

- Hyperliquid Founder Jeff (Public Statements)

- Glassnode (Open Interest Analysis)

- Coinglass Liquidation Heatmap

- Truth Social (President Donald Trump)

- MetaFinancialAI (On-chain analysis of Binance wallets)

- SlowMist

- The New York Times

- Cointelegraph (ETH selling reports)

- EGA Crypto

Disclaimer:This article is for informational purposes only and should not be considered financial advice. Please do your own research before making investment decisions.