This article will meticulously analyze the value of the UNI token by examining Uniswap's operational landscape during 2024-2025, providing insights into its future trajectory. Since its inception in 2017, Uniswap has steadfastly maintained its pioneering role in the decentralized finance (DeFi) sector, not merely as the largest Automated Market Maker (AMM) protocol on Ethereum, but also as a crucial infrastructure developer for the entire DeFi ecosystem. Notably, through its UNI governance token, Uniswap has established a sustainable value distribution mechanism for its community of users and token holders. As the blockchain industry enters an unprecedented period of strong innovation in 2024-2025, protocols are no longer just competing on product offerings, but also on infrastructure and user experience.

Redefining DeFi: Three Core Trends

Three primary trends are currently reshaping the DeFi landscape:

- The Rise of Decentralized Stablecoins: A new generation of stablecoins such as USDe (Ethena), USDS (MakerDAO), and USDY (Ondo Finance) are emerging as the backbone of DeFi liquidity, gradually replacing the roles of USDT and USDC in lending protocols, AMMs, and derivatives exchanges. This shift signifies a move towards more decentralized and potentially censorship-resistant forms of stable value within the crypto economy.

- Cross-Chain Wave and Distributed Liquidity Layers (DLL): The market is rapidly moving towards bridge-less DEX models and global liquidity layers, breaking free from single-chain limitations. This allows for seamless asset transfers and trading across different blockchains without the need for traditional, often vulnerable, bridges. The goal is to create a truly interconnected and liquid multi-chain ecosystem.

- Modular Blockchains and App-Specific Chains: Large DeFi applications are moving away from relying solely on Ethereum or general-purpose Layer 2s to build their own dedicated blockchains. Utilizing frameworks like OP Stack (Optimism), Polygon CDK, or Arbitrum Orbit, these app-specific chains offer greater control over costs, user experience (UX), and performance. This modular approach allows DeFi protocols to tailor their underlying infrastructure precisely to their needs, optimizing for specific use cases and fostering bespoke blockchain environments.

Throughout its nearly a decade of leading the DeFi industry, Uniswap has witnessed continuous market evolution, from the DeFi Summer of 2020, the emergence of new-generation AMMs, to the advent of Layer 2 blockchains and bridge-less cross-chain models. However, these very changes have also presented Uniswap with unprecedented challenges.

While in its early stages, Uniswap only needed to focus on optimizing its core product—a simple AMM protocol on Ethereum—by 2024, that was no longer sufficient. The very nature of the industry has changed:

- Low transaction costs have become the standard, no longer a competitive advantage.

- Users demand a multi-chain experience with high speed and optimized costs.

- Developers require a flexible architecture that allows for customized trading logic, rather than being confined to the traditional AMM model.

To maintain its competitive edge, Uniswap has been compelled to undergo a self-transformation, not as a standalone protocol, but as a comprehensive suite of products and infrastructure. This holistic approach simultaneously addresses three core issues: liquidity, scalability, and customizability. It is precisely for these reasons that over the past two years, the Uniswap Foundation has launched a series of groundbreaking initiatives aimed at further solidifying its position as a leading DeFi protocol in the market. These initiatives also seek to expand revenue streams from its business model and generate direct revenue for those who believe in Uniswap's vision, such as UNI holders and stakers. Among these, the most notable include:

- The launch of Unichain

- Uniswap v4 with Hooks

- UniswapX and UniswapX V2

This transformation not only helps Uniswap maintain its competitiveness in the era of Layer 2s and cross-chain operations but also unlocks opportunities for sustainable revenue growth from both its products (Uniswap v4, Hooks, UniswapX) and its operational infrastructure (Unichain). The direct impact of these strategic moves on investors who believe in Uniswap's long-term vision is a key focus of this analysis.

Unichain's Current Status: Challenges and Achievements

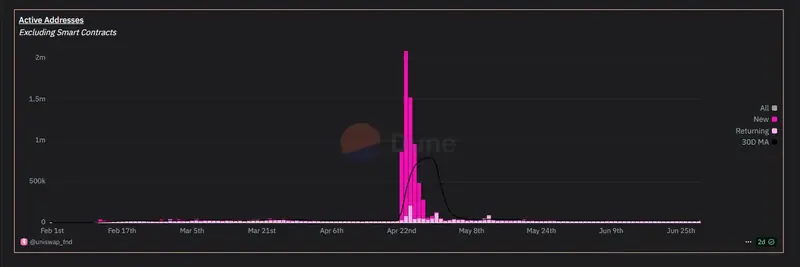

Layer 2 Unichain, launched in February 2025, utilizes OP Stack technology, part of the Superchain ecosystem, to provide fast transactions with an initial block time of 1 second, projected to decrease to 250 milliseconds. This network is designed to become a hub for DeFi and cross-chain liquidity, with strong backing from major projects like Circle, Coinbase, Lido, and Morpho.

In 2024, Unichain commenced with its testnet in October 2024, processing 50 million transactions and deploying 4 million smart contracts, achieving an uptime of over 99%. By 2025, after its mainnet launch in February, Unichain rapidly grew thanks to incentive programs designed to foster its ecosystem.

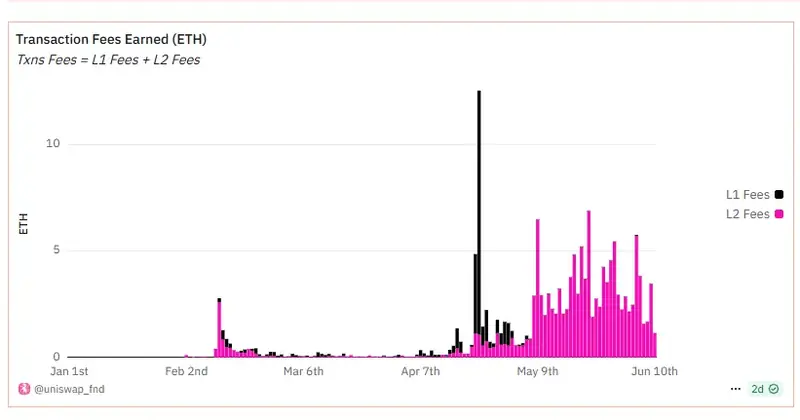

Unichain generates revenue primarily from transaction fees, including base fees, priority fees, and Maximal Extractable Value (MEV). A portion of this revenue is used to cover data posting costs to Ethereum (L1), and the remainder (net revenue) is distributed to validators contributing to Unichain's operation and to UNI token stakers. Specifically, 65% of net revenue is allocated to stakers. At Unichain's launch, this was estimated to provide annual revenue for UNI stakers ranging from $16 million to $33 million, based on trading volume and comparisons with other L2 networks like Base.

So, five months since Unichain's official mainnet launch, are the actual figures reflecting these initial projections from Uniswap?

Unichain's Current Problems

Despite receiving strong backing from strategic partners like Circle, Coinbase, Lido, and Morpho, Unichain is facing a concerning reality: user growth is significantly slower than anticipated. Since its mainnet launch, daily active users (DAU) have only maintained around 30,000, with an average of only about 2,000 new users per day. These figures indicate that Unichain's market reach and penetration remain very limited, especially when compared to the initial expectations of the community and Uniswap Labs itself.

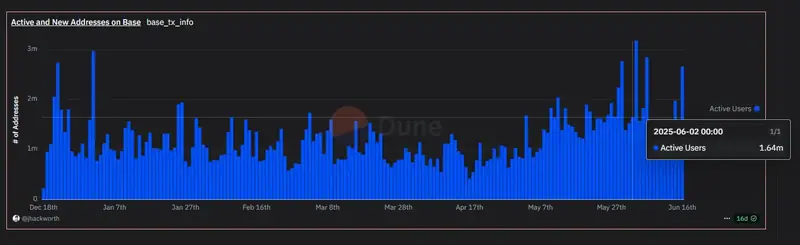

Meanwhile, Base, the Layer 2 operated by Coinbase, is demonstrating a significant lead across almost all growth metrics. Base consistently maintains an average of 1.6 to 2 million daily active users, attracts over 100,000 new users daily, boasts an ecosystem with over 400 developing projects, and achieves net profits of up to $125 million per year, equivalent to approximately $130,000 in weekly profit solely from transaction fees.

Conversely, Unichain is currently only generating revenue fluctuating around 2-3 ETH per day, equivalent to approximately $10,000—a very small figure when compared to Base or other top Layer 2s like Arbitrum or Optimism. This outcome directly leads to the shared revenue for UNI stakers and Unichain validators remaining extremely limited, insufficient to create an attractive value stream for investors who believe in Uniswap's revenue-sharing model.

The disparity is not only in financial metrics but also clearly reflected in growth strategies. While Base fully leverages Coinbase's enormous user base to generate strong traction for its on-chain ecosystem, Unichain, with its "DeFi infra for DeFi" model, is overly reliant on the DeFi community, which is gradually saturating and growing significantly slower than the retail user influx from Web2 or CeFi. This reality poses a big question for investors: Can Unichain's strategy of building a central infrastructure layer for DeFi be attractive enough and fast enough to catch up, especially given that its competitor, Base, is dominating market share through a mass adoption strategy, effectively utilizing the bridge between the centralized and decentralized financial worlds?

Without decisive adjustments to its product, user experience, and builder acquisition strategy, Unichain risks becoming merely an auxiliary Layer 2 for the Uniswap ecosystem, rather than a true DeFi liquidity hub as originally envisioned.

However, it's still important to acknowledge that despite the challenges in user growth and revenue, Unichain has achieved some significant milestones in terms of liquidity infrastructure. Specifically, in just under 5 months since mainnet, Unichain has officially surpassed the $800 million TVL (Total Value Locked) mark, with over 50% coming from stablecoins. This indicates that the ecosystem is gradually becoming a stable liquidity center for DeFi protocols, especially applications revolving around stablecoins and risk-free yield models. This is a positive signal reflecting confidence from liquidity providers and large DeFi protocols, despite retail user adoption not meeting expectations.

Uniswap v4: A Promising Upgrade?

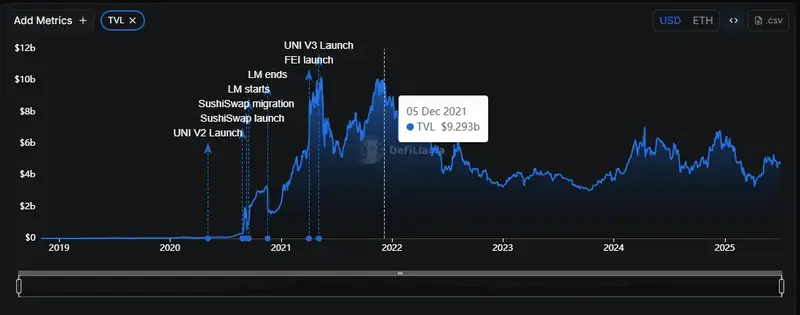

Since its launch in May 2021, Uniswap v3 created a major turning point in the DeFi industry with its "concentrated liquidity" mechanism, allowing liquidity providers (LPs) to focus capital into specific price ranges instead of spreading it across the entire price spectrum as in previous versions. This mechanism immediately significantly improved capital efficiency and became the foundation that helped Uniswap v3 maintain its market-leading position for nearly four years.

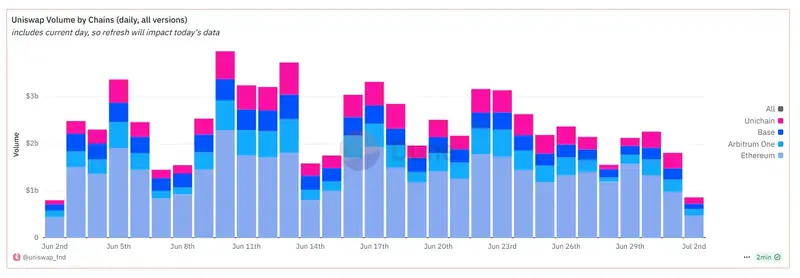

In fact, Uniswap currently processes about $3.3 billion in daily trading volume, equivalent to 23% of the global DEX market share, leading the market.

This figure is also confirmed by DeFiLlama with similar statistics, showing Uniswap holding its #1 position with approximately $3 billion/day in trading volume, far surpassing its closest competitor, PancakeSwap, with $2.7 billion and 21% market share.

However, despite its dominance in trading volume, Uniswap's current Total Value Locked (TVL) fluctuates around $5 billion, less than half of its 2021 peak. This reflects a general trend across the entire DeFi market, where industry-wide TVL remains relatively low compared to its peak, estimated to range from $124 billion to $132 billion.

In this context, Uniswap v4, officially announced in January 2025, is expected to be a pivotal upgrade, not only building on v3's success but also helping Uniswap adapt faster to market changes and the increasingly high demands from its user and developer communities. The biggest highlight of v4 is its ability to expand and customize its infrastructure, aiming to position Uniswap not merely as an AMM, but as a comprehensive liquidity infrastructure platform or a "DeFi Liquidity Operating System."

The core of Uniswap v4 is its Hooks mechanism, which allows custom code snippets to be embedded at specific points in a pool's lifecycle. This includes moments from initialization, when LPs add or remove liquidity, and before or after each swap. Hooks transform each liquidity pool into a highly programmable module, where developers can build mechanisms like dynamic trading fees, limit orders, TWAP orders, or even reuse out-of-range liquidity to deploy into lending protocols, thereby generating additional profit streams. This is a significant leap forward compared to the rigid pool model of previous versions. Statistics after more than 6 months since its launch show that over 1,600 different Hooks have been deployed on Uniswap v4, with total accumulated trading fees across all chains reaching nearly $30 million.

Besides Hooks, v4 also introduces a critical infrastructure change called "The Singleton." While in previous versions, each trading pair on Uniswap had to deploy a separate smart contract, with Singleton, all pools will be consolidated into a single smart contract. This approach not only optimizes gas costs, especially in complex multi-step transactions, but also reduces the cost of deploying new pools by up to 99%, allowing builders to create new trading pairs at virtually no cost. Singleton also integrates a "flash accounting" system, which only transfers the net difference after a transaction is completed, instead of moving all assets throughout the swap process as v3 operates. This significantly reduces gas fees for end-users.

However, the question remains whether Uniswap v4 will truly achieve its expectation of becoming a new growth lever for the Uniswap ecosystem, similar to what v3 did in 2021, and whether it will genuinely deliver actual value to investors who believe in UNI's vision.

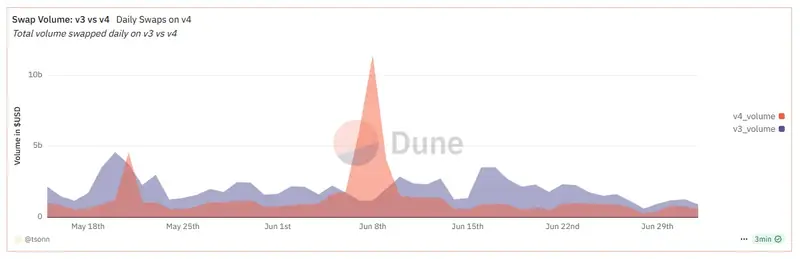

When observing actual operational metrics, after 6 months since its launch, Uniswap v4 currently only records daily trading volume equivalent to about 35–50% of Uniswap v3, indicating that market adoption is still quite limited.

In terms of liquidity, although v4's TVL has for the first time surpassed $1 billion, equivalent to about 20% of Uniswap's total TVL, this figure is still quite modest compared to v3's TVL, which currently maintains around $2.3 billion, accounting for nearly 48% of the total TVL.

Beyond market factors, some barriers preventing Uniswap v4 from breaking out may stem from concerns about smart contract risks related to the use of Hooks. These custom code snippets inherently carry the potential for bugs or exploitation if not thoroughly audited. Concurrently, from a builder's perspective, accessing existing liquidity has become more challenging because v4 and v3 are distinct ecosystems at the infrastructure level, not directly sharing liquidity. Additionally, in a market that has not yet strongly recovered, investors and LPs adjusting their capital flow strategies are also factors contributing to v4's growth not meeting expectations.

However, it is important to recognize that despite the challenges in user growth and revenue, Uniswap v4 has achieved some important milestones in terms of liquidity infrastructure.

Through this v4 update, investors holding UNI or UNI stakers will directly benefit from the expansion of Uniswap's business model. To date, Uniswap has primarily generated revenue from collecting fees on swaps within its pools. However, these fees are, by default, allocated to liquidity providers (LPs) rather than the protocol or token holders. A proposal to redirect a portion of this revenue from LPs to the treasury or UNI stakers has been discussed since 2023 but has not yet been officially implemented.

With Uniswap v4, Uniswap's revenue model has the potential to expand through three new drivers:

- Hooks-as-a-Service: Hooks are not just technical tools but can also be commercialized. For example, Uniswap Labs or third parties could develop premium Hooks (e.g., TWAP engine, boosted yield, dynamic fees) and charge license fees or usage fees for these Hooks. If this mechanism becomes standard, it could unlock entirely new revenue streams not dependent on traditional trading fees.

- Reduced Operational Costs for LPs, Stimulating Liquidity Growth: Singleton and Flash Accounting reduce gas fees by up to 99% for new pools and 15-20% for average swap transactions, thereby incentivizing more new LPs to join. Higher TVL leads to lower spreads, which helps increase overall trading volume, indirectly boosting revenue from swap fees.

- Fee Switch Mechanism: The Fee Switch (sharing trading fees with the protocol or stakers) is highly likely to be activated synchronously with v4's widespread adoption. With Hooks and Singleton enhancing customizability and cost savings, opposition pressure from LPs will also be much lower than with v3.

If the Fee Switch is activated with a 10-20% share of swap fees, based on an average daily trading volume of $3.3 billion, Uniswap could generate from $3 million to $6 million in trading fees per month (equivalent to $36 million – $72 million per year) from v3 and v4 alone. If v4 continues to grow and surpasses v3, this figure could double.

With an allocation mechanism similar to many current L2s (e.g., Base allocating 65% to stakers, 35% to treasury), UNI stakers could potentially expect actual income ranging from $23 million to $47 million per year, not including revenue from Hooks or other fee models.

The potential APY for UNI stakers ranges from 5%-10% depending on the level of lock-up and the total amount of UNI participating in staking (estimated at 30-50% of the total circulating supply). If operational metrics, including trading volume, TVL, user count, and especially the adoption rate of Hooks on Uniswap v4, continue to maintain growth momentum or even improve significantly in the near future, this could fundamentally transform the UNI token. Specifically, the UNI token is highly likely to evolve from merely a Governance Token, where the primary right is to participate in DAO voting, into a Cash-flow Token that provides actual revenue streams for holders in the long term.

UniswapX and the Trend of Intent-Based Trading

Why is intent-based trading gaining so much attention? Imagine you're a DeFi trader wanting to swap token A for token B, but liquidity is fragmented across multiple chains and protocols. This forces you to manually find the best execution path, pay gas fees, and face the risk of front-running. This is the reality many DeFi users have experienced.

The trend of intent-based trading emerges as a solution, allowing you to simply sign your "intent" for a transaction, such as "I want to swap 100 USDC for ETH at the best price," and the system automatically finds a way to execute it. Research shows this trend is driven by:

- Liquidity Fragmentation: With the development of Layer 2s and new AMMs, liquidity is fragmented, making it complex to find optimal prices.

- Gas Costs: UniswapX eliminates gas fees for users, shifting the burden to "fillers" (executors), thereby reducing financial barriers.

- MEV Protection: It reduces the risk of front-running through private relays, protecting users from sandwich attacks.

- User Experience: It simplifies the process, making DeFi more accessible, similar to trading on Centralized Exchanges (CEXs).

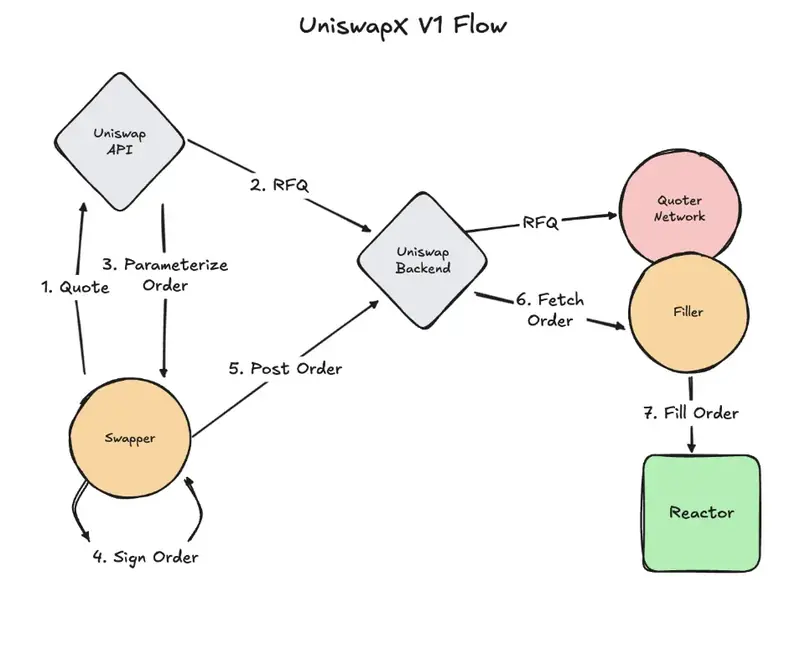

This story is not just about technology; it's about meeting the growing demands of the DeFi community. Protocols like CowSwap and 1inch Fusion have pioneered this space, compelling Uniswap to act to avoid being left behind. Not one to be left out, in July 2023, Uniswap Labs officially launched UniswapX—a completely new trading architecture that lays the foundation for Uniswap's participation in the "intents revolution."

With UniswapX, users no longer need to pay gas or find optimal matching paths. Instead, they simply sign an off-chain "intent," and a network of solvers (transaction executors) compete to execute that order at the best rate—from any liquidity source (DEX, CEX, aggregator...). The solver that performs best is chosen to execute the transaction and receives a corresponding reward.

UniswapX v1: Initial Impact

UniswapX v1 immediately gained traction due to its outstanding features:

- No gas fees for users; the solver bears the cost.

- Reduced MEV as orders are matched off-chain before being executed on-chain.

- Better prices due to competition among solvers.

- Seamless, user-friendly experience for the general public.

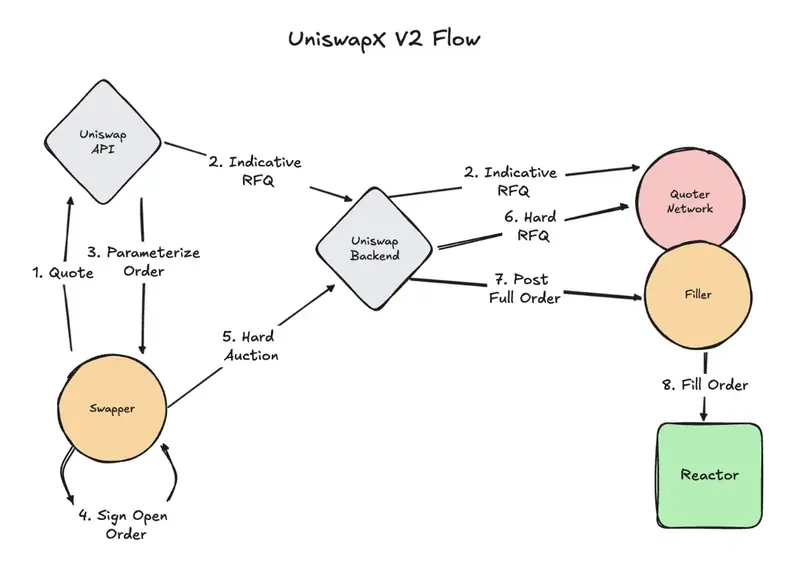

Just over a year later, UniswapX received its first major upgrade: UniswapX v2, designed for compatibility and to fully leverage the power of Uniswap v4 and its Hooks architecture. While v1 was the first step towards intents-based swaps, v2 is where those ideas are elevated to a comprehensive infrastructure level.

Key Highlights of UniswapX v2

- Deep Integration with Hooks: Allows for custom trading logic using custom code snippets—for example, KYC checks, volume limits, MEV reduction... all of which can occur directly within the swap process.

- RFQ Pools (Request-for-Quote Pools): Now, market makers (LPs) can participate in auction-style pools where they provide real-time quote rates, directly competing to fill intents. This helps create a much more efficient liquidity market than traditional AMMs.

- Cross-Chain Intents: UniswapX v2 isn't limited to Ethereum—it's designed to expand to multiple other chains through bridging solutions like Chainlink CCIP, LayerZero, or Wormhole. Users can swap from a token on Chain A to a token on Chain B without complex manual operations.

- Smart Gas Fee Auctions: Solvers can bid flexible gas prices—users not only don't need to pay gas, but they can even receive a portion of the rebate from the solver if market competition is high enough.

Uniswap's transformation with UniswapX v2 is not merely a technical update. Uniswap is no longer just a decentralized exchange based on the AMM formula; it is gradually becoming the intents engine infrastructure platform for the entire DeFi ecosystem. In this new world:

- Users simply express what they want.

- The infrastructure automatically finds the best way to achieve it.

- Solvers, LPs, CEXs, and DEXs become "workers" competing to fulfill user intents.

Where Does UniswapX Stand in the Race?

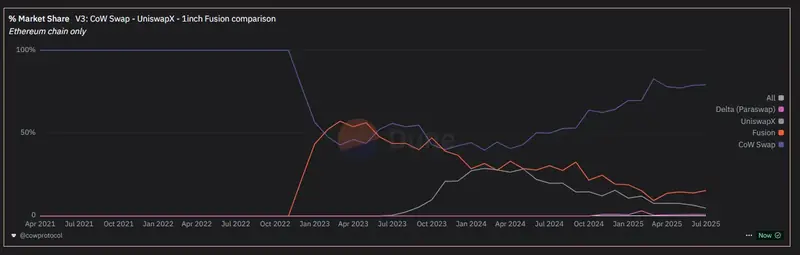

Since its official launch, UniswapX has recorded over $22 billion in trading volume, corresponding to $66 million in collected trading fees (equivalent to 0.3% fee collected per transaction through UniswapX).

However, at present, UniswapX is still struggling to compete for DEX aggregator market share with CoWswap, Fusion (1Inch), and Paraswap. UniswapX currently holds only 4.7% of the market share, while CoWswap leads with 79% and 1Inch Fusion follows with 15%.

Although it holds only ~4.7% of the intents market share, the $22 billion trading volume is still highly significant:

- Proof of Utility: This is evidence that the motivation to use UniswapX is real, especially since the Uniswap ecosystem remains the most accessed platform in DeFi.

- Foundation for Fee Switch: This volume creates an extremely important prerequisite for UniswapX to activate the fee switch for $UNI in the future—if governance approves.

- Native Integration Advantage: The majority of UniswapX's volume comes from native integration into the Uniswap interface. This suggests that if properly promoted (e.g., through incentives, UI pushes, or solver benefits), UniswapX's market share could rapidly accelerate.

UniswapX v2 is expected to be Uniswap's "strategic answer" to the increasing competitive pressure:

- Hooks will unlock a world of customization that CoWswap and 1inch Fusion struggle to replicate (as they don't control the original AMM).

- RFQ Pools will help UniswapX attract professional LPs, thereby competing on rates and large volumes.

- Cross-chain intents could be a "strategic weapon" if UniswapX expands to support popular Layer 2 chains.

Although UniswapX still holds a modest position in the intent-based trading market share ranking, it is far from being out of the game. On the contrary, with over $22 billion in volume achieved in just one year, UniswapX proves that by combining the right infrastructure (v4 + Hooks) and the right expansion strategy (RFQ + cross-chain), UniswapX can absolutely transform from a "late mover" into a "category leader." While CoWswap dominates with its first-mover advantage and middleware, and 1inch Fusion boasts RFQ power and a large user base, UniswapX possesses something no one else does: a foundational AMM that is #1 in the market, and an unprecedented suite of infrastructure tools (Hooks) in DeFi.

$UNI's Role in Uniswap's Value Structure

In a rapidly evolving DeFi landscape driven by three major trends (fragmented liquidity, intent-based trading, modular blockchains), Uniswap is not simply "keeping up," but is actively redefining itself from an AMM into a comprehensive liquidity infrastructure ecosystem. From Unichain (its own Layer 2), Uniswap v4 (Singleton + Hooks), to UniswapX (intent-based engine), these are no longer standalone products but strategic pieces aimed at a unified Uniswap, optimized for all liquidity needs within DeFi.

Model for UNI token value creation.

For over four years, UNI has been a symbol of the governance token model, where investors held voting rights but received almost no actual cash flow from the ecosystem they helped build. However, the 2024-2025 period marks a historic turning point for Uniswap—not just in product direction, but, more importantly, in the mechanism for distributing value back to those who believe in the protocol's long-term vision.

Crucially, all of these models enable revenue mechanisms that can be directly distributed to UNI stakers, signaling a clear progression from a "governance token" to a "cash-flow token." This fundamental shift will likely make UNI a much more attractive asset for long-term investors seeking tangible returns from the Uniswap ecosystem.

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Please do your own research before making investment decisions.