Continuing the analysis of AAVE from Part 1, this article focuses on the key components shaping the Aave ecosystem and evaluates the project's tokenomics.

The Components Shaping the Aave Ecosystem

After years of establishing its position in the lending sector, Aave is working to expand its business model beyond collateralized lending to become a complete Web3 financial ecosystem. Beyond just providing liquidity, the new products developed by its parent company, Avara, show a vertical integration strategy, from user infrastructure and asset flows to the on-chain social layer, with products including:

- Stablecoin (GHO)

- New revenue distribution model (Anti-GHO)

- Institutional platform (Aave Arc)

- Decentralized social network (Lens Protocol)

- Consumer-focused wallet infrastructure (Family Wallet)

GHO Stablecoin: Aave's Core Asset Infrastructure

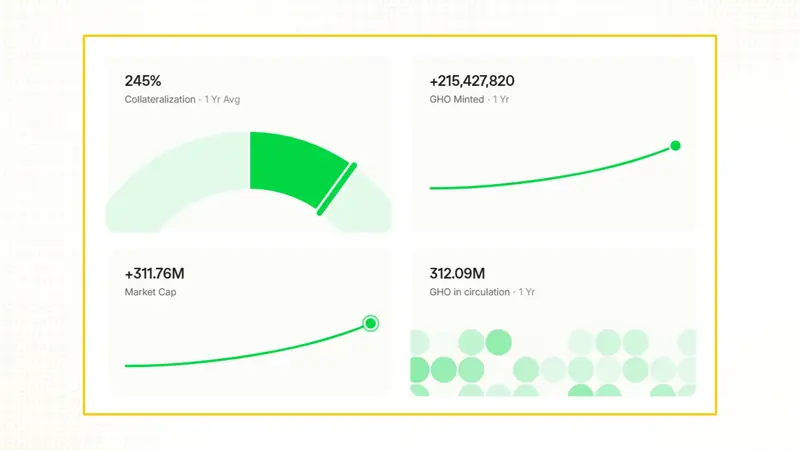

A financial ecosystem struggles to grow without a native stable asset. For Aave, this is materialized through GHO, an overcollateralized stablecoin similar to MakerDAO's DAI model, but integrated directly into the lending protocol. Users can mint GHO by locking assets on Aave, with an interest rate adjusted by the DAO. The interest collected from the minting process is not paid to LPs like with regular loans, but goes directly to the DAO treasury, creating a revenue stream separate from the traditional lending model.

A notable mechanism is that users who stake AAVE in the Safety Module receive a preferential interest rate when borrowing GHO. This creates an incentive flywheel: stake AAVE → reduce GHO minting fees → increase demand for GHO → increase revenue for the DAO → enhance the value of AAVE. According to data from mid-2025, over 200 million GHO have been minted since its launch, with a market capitalization of over $300 million. This is equivalent to approximately 0.11% of the total stablecoin market size, a modest figure compared to its goal of competing with top stablecoins. The adoption of GHO will heavily depend on its ability to integrate with external DeFi protocols and the market's trust in its decentralized minting model, especially as stablecoins are a focal point for both regulatory and investment activity in the second half of 2025.

Anti-GHO: A New Revenue Distribution Model for AAVE Stakers

Anti-GHO is a non-transferable ERC-20 token issued through the Merit system to users who stake AAVE and StkBPT. The goal of Anti-GHO is to create a clearer and more transparent tool for sharing GHO revenue. Anti-GHO has two main functions: it can be used to burn at a 1:1 ratio with GHO debt, helping users reduce their debt obligations without incurring additional costs. It can also be staked to earn incentives similar to interest, and after a cooldown period, it can be redeemed for GHO. A key detail is that 50% of the revenue from GHO will be converted into Anti-GHO, and 80% of this Anti-GHO will be distributed to AAVE stakers. With estimated GHO revenue of approximately $12 million/year (based on an APY of ~6.45% and a supply of ~186 million GHO), this mechanism could generate about $6 million in Anti-GHO value annually, which is then redistributed to the staking community. In essence, this is a shift from a personal discount rate model to a collective revenue-sharing model, which extends benefits to even those who stake AAVE but don't borrow GHO. This helps increase the attractiveness of StkAAVE as a staking asset with a cash flow directly tied to the protocol's performance.

Aave Arc: Connecting DeFi to Institutional Capital

To solve regulatory challenges and attract institutional capital, Avara has implemented Aave Arc—a version of the lending protocol exclusively for KYC-verified parties. Unlike the standard decentralized model, Aave Arc requires all participants to be pre-verified, including liquidity providers and borrowers. The idea behind Aave Arc is to bring DeFi closer to traditional financial institutions while creating a more stable revenue stream from fees and interest on a large scale. Additionally, having a compliant version also helps the Aave ecosystem enhance its legitimacy, opening up opportunities for partnerships within existing regulatory frameworks. However, in practice, Aave Arc has not yet gained significant traction. Factors such as a lack of liquidity, complex due diligence processes, and unclear performance have prevented Arc from becoming the DeFi-TradFi bridge it was originally envisioned to be. This remains a promising experiment, but it requires many adjustments to prove its long-term effectiveness.

Lens Protocol: The SocialFi Approach

Beyond financial products, Avara is also investing in Lens Protocol, a decentralized social media platform where every interaction (post, follow, comment) is tokenized into a tradable NFT. Users can create content and earn income through tipping, sponsorships, or other decentralized advertising models. With its focus on connecting social and financial activity, Lens opens a new path for DeFi, where social behavior data can be integrated into credit systems or future lending models (Social Credit Layer). This not only diversifies data sources but could also create new forms of non-traditional risk assessment. While Lens is still in its early stages of development and its user base is limited compared to Web2 social networks, the launch of Lens Chain, a dedicated blockchain for SocialFi applications, shows Avara's long-term ambition to expand DeFi's boundaries into the social, content, and digital identity space.

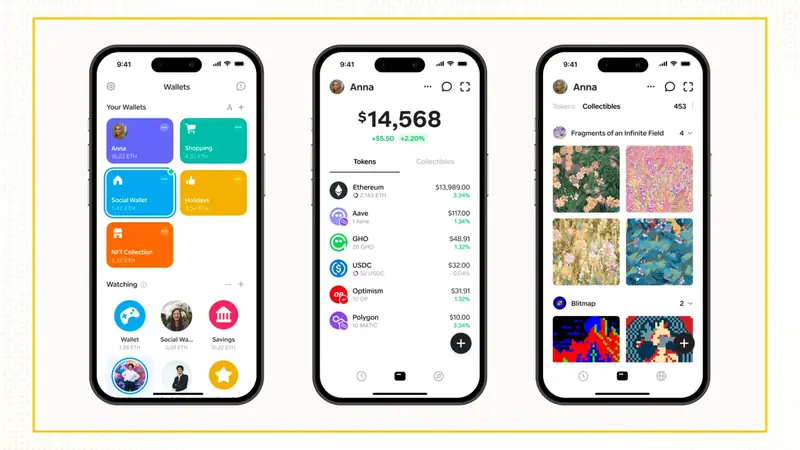

Family Wallet: Infrastructure for the End-User

In addition to developing core financial protocols, Avara is expanding into the user experience segment with Family Wallet—a smart contract wallet designed to simplify interaction with DeFi. Instead of requiring users to remember a seed phrase, understand transaction signing mechanisms, or pay gas fees, Family Wallet hides most of the technical layers, bringing the experience closer to Web2 financial applications. The wallet directly integrates key products within the Aave ecosystem such as minting GHO, staking AAVE, accessing Aave Markets, and interacting with Lens Protocol.

Consolidating all services into a single interface reduces the barrier to entry for newcomers while enabling the deployment of freemium models, staking incentives, or service fee mechanisms. Although Family Wallet is still in the development and testing phase, this direction shows that Avara is building a bridge between the average user and Web3 financial products—a crucial condition for long-term ecosystem growth.

AAVE as the Binding Force of the Ecosystem

All the products mentioned above revolve around or are connected to AAVE:

- Staking AAVE to receive rewards and reduced GHO borrowing interest rates increases staking demand. Revenue from GHO minting and protocol interaction flows back to the DAO, accumulating internal value.

- Aave Arc collects institutional fees and expands the legal-friendly network, leading to potential for larger cash flow development.

- Lens Protocol can implement a usage fee model based on token gating or NFT minting fees, creating a new revenue stream from SocialFi activities or even InfoFi.

- Family Wallet becomes a distribution channel for DeFi services with fees or incentives for AAVE stakers, contributing to increased benefits for AAVE holders/stakers and encouraging users to accumulate the token.

All of these circles connect to form a closed ecosystem of assets, liquidity, social interaction, and institutions, where users at any point can be led back to the core protocol, Aave, and the AAVE token.

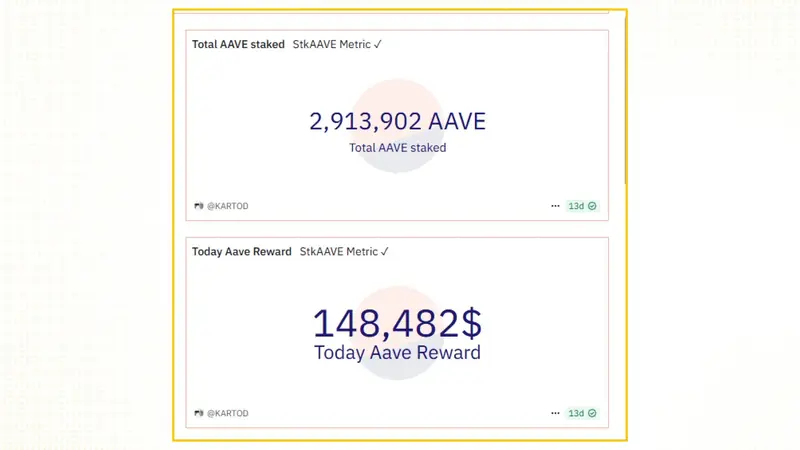

Currently, nearly 3 million AAVE tokens are staked directly in the protocol and the Safety Module. Concurrently, the Aave DAO is also distributing approximately $150,000 worth of rewards weekly to StkAAVE holders. This figure demonstrates the real-world connection between token holders and the protocol's activities. This expansion is not just about product diversification; it is a strategy to close the loop on the Web3 financial value chain. Investors should view Aave as a financial infrastructure layer, which not only dominates the lending market but also creates a self-sufficient digital asset ecosystem.

Aavenomics: Redefining AAVE's Value

In the ecosystem structure of Aave and its parent company Avara, the AAVE token holds a central role, not just at the governance level but as the binding mechanism between products. From traditional lending activities to expanded models like GHO, Aave Arc, Lens Protocol, or Family Wallet, all have operational elements that revolve around or directly interact with AAVE.

For example, users stake AAVE to receive staking rewards and simultaneously get a reduced GHO borrowing interest rate. Products like GHO, Aave Arc, or Lens all generate revenue for the DAO, and a portion of this profit is accumulated in the Treasury—where AAVE holders have the right to vote on how it is distributed through governance.

Notably, AAVE is the successor to the LEND token—the original token of the EthLend platform. Initially, LEND had a total supply of 13 million LEND. However, after rebranding to Aave, the project migrated LEND to AAVE at a 1:1 ratio and planned to increase the circulating supply by an additional 3 million AAVE, bringing the total supply to 16 million AAVE. This also marked the point when the Aave ecosystem entered its maturity phase, repositioning itself as a multi-chain lending protocol rather than just a standalone dApp.

As of mid-2025, over 94% of the AAVE supply has been unlocked (equivalent to ~15,040,000 tokens). Only about 960,000 AAVE (~$288 million) will be gradually distributed over the next 26 months (until September 2027). With an average unlock rate of approximately $11 million/month, this dilution is very low compared to Aave's current market capitalization and liquidity.

Furthermore, according to data from Dune (@KARTOD), nearly 3 million AAVE are currently staked directly, and the Aave DAO is distributing ~150,000 USD weekly in rewards to StkAAVE holders. This figure shows the real-world connection between token holders and the protocol's activity.

Aavenomics: Redefining AAVE's Token Utility

In recent proposals like Aave 2030 and Aavenomics Implementation, a clear direction for redesigning AAVE's utility is visible. Instead of just a governance token, AAVE is gradually becoming the center of a "stake-to-earn" revenue distribution model, where stakers provide system security and receive rewards commensurate with their contribution. The upcoming deployment of Aave v4 further reinforces this positioning. Additionally, the Aave DAO has launched a Buy and Distribute program, with a plan to buy back AAVE from the secondary market at an initial rate of $1 million/week for the first 6 months. The repurchased tokens will be deposited into the Ecosystem Reserve, to be used for staking rewards, development activities, or user incentive programs. Starting in 2025, this program will be adjusted quarterly, with a long-term goal of fully offsetting the amount of AAVE spent during operations. This is a notable step in building a circular value model, where revenue returning to the DAO is redistributed to the community in a transparent and strategic manner.

Valuation Perspective: Is AAVE Undervalued?

According to data from CoinGecko (July 2025), AAVE is currently trading around $300-$330, with a Fully Diluted Valuation (FDV) of over $5 billion. However, if only the truly circulating supply is considered (excluding staked and treasury amounts), the actual market cap is only about $3.5 billion. With a TVL-to-market cap ratio of 8.85x, plus an estimated revenue of over $100 million/year, the current valuation could be considered low compared to the cash flow performance of the Aave ecosystem. This is a metric that many investors are watching closely, especially as top DAOs increasingly focus on transforming governance tokens into assets that generate stable revenue streams.

Aave's Operational Performance in Mid-2025

As of mid-2025, data from DefiLlama and Aave Analytics record many positive metrics for the Aave ecosystem:

- TVL reached $30 billion, an increase of nearly 50% year-over-year, reflecting stable growth despite market volatility.

- Net deposits reached $50 billion, showing a high level of user trust in locking capital into the protocol.

- Total outstanding loans reached $16.83 billion, accounting for ~47% of the DeFi lending market share, far surpassing platforms like Compound, Spark, or Morpho.

- DAO revenue in 2024 was estimated at over $73 million, primarily from borrowing fees and flash loans.

- Nearly 2.3 million wallets have interacted with Aave across more than 7 blockchains, including Ethereum, Arbitrum, Optimism, Polygon, and Base.

From an infrastructure investment perspective, Aave now possesses three notable pillars: deep liquidity, multi-chain scalability, and a clear value accumulation mechanism. This is a relatively rare structure in the DeFi space, where most protocols only optimize for one or two factors.

Competitive Landscape in DeFi Lending: Beyond TVL

Aave's strong growth in the first half of 2025—from TVL, revenue, to user count—shows that the protocol is operating as a true "infrastructure pillar" in the decentralized lending market. However, to better understand Aave's position, it's necessary to place it within the current competitive landscape, where DeFi lending economic models are gradually diverging.

Compound: Efficient Protocol, but Limited Value Distribution

Compound was the first project to introduce a decentralized lending market model, where borrowers and lenders interact through liquidity pools similar to Aave. However, the difference lies in its revenue model and value distribution. Compound generates revenue from borrowing fees via a dynamic interest rate, but most of this revenue is left for liquidity providers rather than flowing to the treasury. The treasury receives a very small portion, and the COMP token, despite its governance role, does not provide direct economic benefits to holders. Because of this, Compound's economic model struggles to create long-term incentives for holding COMP, and it also fails to generate an internal flywheel like Aave, where users are both incentivized to participate in the protocol and have a clear mechanism for defense and income.

Morpho: A Revolution in Efficiency, but a Challenge in Revenue Model

Morpho takes a completely different approach: instead of using the traditional pool-based model, this protocol "wraps" the liquidity pools of Aave and Compound, and then optimizes lending/borrowing efficiency by performing peer-to-peer matching between borrowers and lenders. As a result, Morpho achieves more attractive interest rates for both sides, reduces slippage, and increases capital efficiency. However, because it operates as an "optimization layer" on top of other protocols, Morpho does not directly own many stable revenue sources. Its current model primarily focuses on growing TVL and improving UX, but it lacks a clear strategy for accumulating value for its DAO or its MORPHO token. The protocol also lacks native products like a stablecoin (Aave's GHO), has no flash loans, and does not implement an internal staking and insurance mechanism like the Safety Module. In other words, while Morpho is very strong in technology and efficiency, to become a protocol that can "stand on its own economically" without relying entirely on TVL or external incentives, it will need to build a native revenue layer and a more specific redistribution structure in the future.

Disclaimer

This article is for informational purposes only and should not be considered financial advice. Please do your own research before making investment decisions.